Equity markets have fluctuated in recent months, but there is a key theme that has developed.

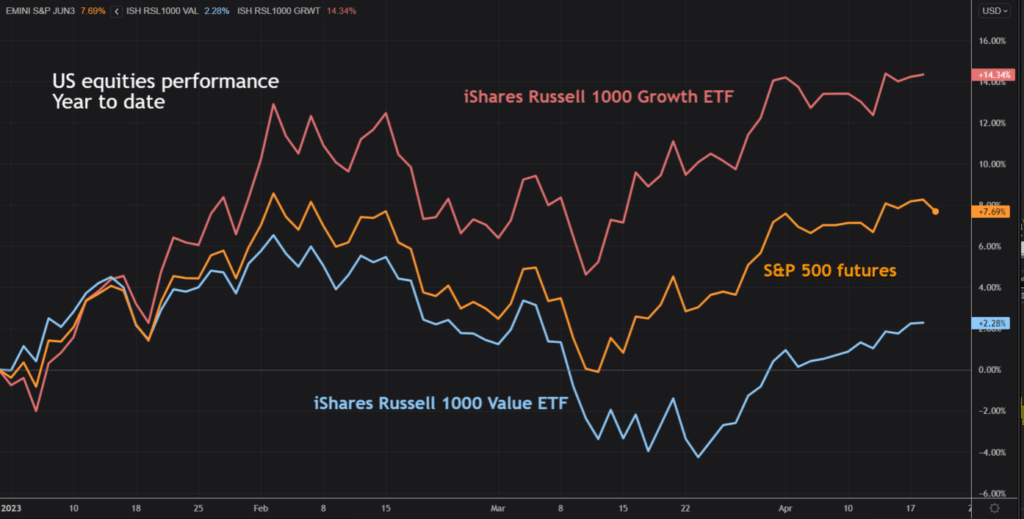

There has been a decisive shift in the outlook for US equities since the turn of the year. US growth stocks have decisively outperformed value stocks.

This has become the key story of US equities so far in 2023.

US growth stocks are storming ahead

In 2023, the big-cap growth stocks have been very strong, whilst the value stocks, well… not so much.

Here’s a list of the year-to-date performance of some of the big-hitting growth stocks in the US:

- Amazon is up c. +22%

- Tesla is up c. +50%

- Meta Platforms is up c. +81%

They are all up strongly. Now, these are just some examples we plucked out of the market. However, these are not isolated examples.

Similarly, let’s now look at some of the more popular value stocks. You will see that they are something of a damp squib.

- Procter & Gamble is flat

- Johnson & Johnson is down c. -9%

- Pfizer is down c. -21%

Once again, this weak performance of the US value stocks is not isolated to my narrow (and arguably a little crude) sample base.

The point I am trying to make is that growth stocks are outstripping the performance of value stocks. Taking a look at the broader market we can see that this is a key theme.

I have used a couple of ETFs for comparison: the iShares Russell 1000 Growth ETF and the iShares Russell 1000 Value ETF. Both have fluctuated, but the contrast in performance is significant. I have also thrown in the S&P 500 futures (which comprise elements of growth and value) to use as a benchmark.

US real yields are key

One of the key reasons why growth is performing so much better than value comes down to interest rates and bond yields. Markets have spent much of 2023 deliberating over the prospect of peak rates by the Federal Reserve. This boils down to two questions for investors.

- “When will the Fed stop hiking?”

- “When will the rate cuts resume?”

Views have swung back and forth for months. However, essentially, the markets are of the view that the Fed is in the final throws of hiking.

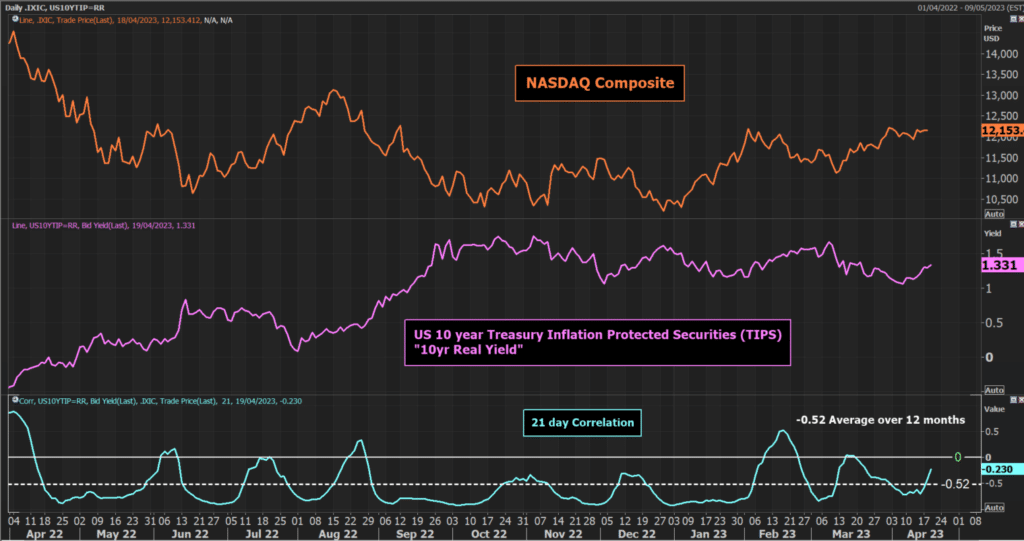

Long-run inflation expectations (on a 10-year basis) have fluctuated between 2.1% and 2.5% but have been broadly ranging. However, bond yields have been in decline. This means that real bond yields (yields minus inflation) have been tracking lower.

This chart of the performance of the NASDAQ Composite and the US 10-year Treasury Inflation Protected Securities (which is effectively seen as the 10-year real yield) shows a very strong negative correlation.

In a nutshell, falling real yields are great for US growth stocks.

Growth stocks perform better during times of falling interest rates. That stands to reason. They usually tend to not pay a dividend. Also, their lofty valuation is not seen as so eye-watering. Amazon for example, currently trades on FY2023 expected multiples of over 70 times earnings.

Can this continue?

So, this then begs the next question. Can this outperformance of growth over value continue?

Well, there are a few things to consider. Volatility has been falling decisively in recent weeks. Since the banking crisis seems to have been alleviated (at least for now), market fears have been receding. This has given growth stocks another boost.

However, the VIX Index (of S&P 500 options volatility) has dropped to around 17 which is the lowest it has been since January 2022. Is the market becoming complacent again?

Also, there are some concerns that the Advance/Decline line on the NASDAQ is lagging. This suggests that maybe it is the bigger hitters that are pulling the market higher. This run higher may not be sustainable.

The current move higher will require US real bond yields to not move decisively higher. Markets seem to be fairly settled on a May rate hike by the Federal Reserve. But in the delivery of this hike, if there is any hint of hawkishness, it could lead to yields pulling higher again. This would be negative for US equities. And as a flip-side to what I noted earlier, this would likely hit US growth stocks (which have had such a strong run higher) the hardest.

A warning not to be complacent

So I will leave you with this. If the recent years following equity markets have taught me anything, it is to guard against complacency. The bull move in US equities has been driven by the growth stocks. This tends to be seen as a sign of normal market conditions.

But there always seems to be a curve ball thrown that jolts investors back to reality. It is always a good idea to be alert and on the guard against complacency. There is nothing worse than buying at the top and then watching it fall!