US equity markets have broken out to multi-month highs. The reasons to not be positive (or perhaps even outright bearish) are still prevalent. Yet, investors still seem happy to climb a wall of worry. Since October, the S&P 500 futures have rallied from a shade above 3500 to hit levels above 4300 this week. However, when I look under the hood, there is a sense of concern that starts to take hold of me. The rally may yet still have legs to run, but a pullback is threatening.

- Volatility continues to slide across asset classes

- S&P futures rallying despite higher real yields

- The lack of market breadth is a significant concern

Climbing a Wall of Worry

There are reasons to be cautious in equity markets. Inflation remains sticky and the US economy continues to throw out data putting it on a path towards recession (despite the labour market remaining solid). There is a slowing recovery of the Chinese economy and geopolitical concerns over the West’s relations with Russia and China.

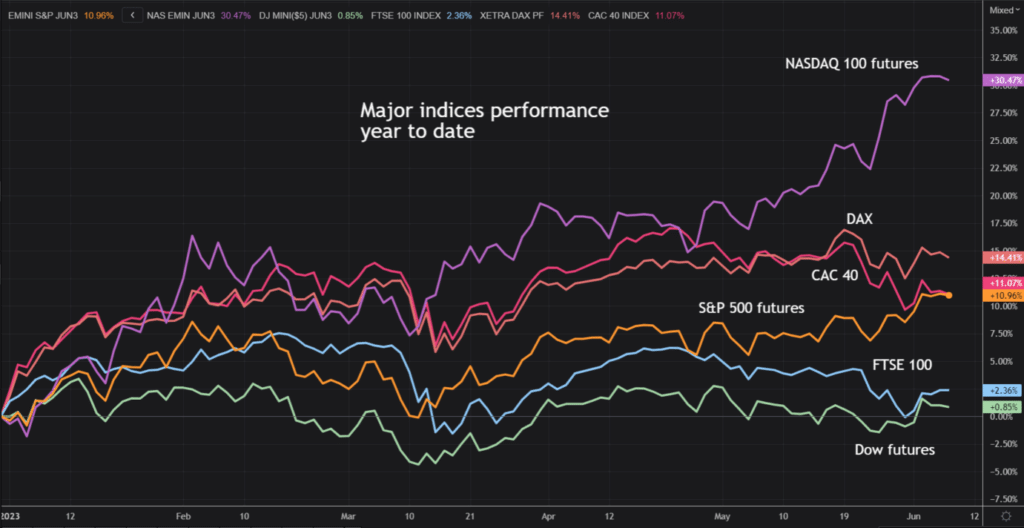

Despite this equity markets have been rallying as investors climb a wall of worry. The e-mini S&P 500 futures and NASDAQ 100 futures have been strong, adding 11% and 30% respectively in the year to date.

However, it is the moves in the past month that have caught my eye, with an acceleration higher. The sustainability of this rally needs to be studied.

Complacency in equities as volatility slides across asset classes

The rally has come amid an incredible reduction in volatility. Here is a breakdown of how volatility gauges across various asset classes have tumbled:

- VIX Index (S&P 500 options volatility) – The CBoE VIX Index fell to below 14 yesterday (although is set to pop a shade higher today). It has not been this low since the pandemic began. Considering the higher levels of interest rates, continued inflation and impending US recession, this is a remarkably low level for implied volatility.

- MOVE Index (Treasury bonds volatility) – Bank of America Merrill Lynch’s bond option volatility index (the bond market equivalent of the VIX) has dropped to its lowest level since mid-February. All of the volatility from the banking crisis has now been unwound.

- Deutsche Bank Currency Volatility Index – Volatility in forex has fallen to levels not seen since February 2022.

The big question is whether this is due to benign conditions in major asset classes that will continue to support rallying risk-on equities. Or whether it portends something more worrying on the horizon.

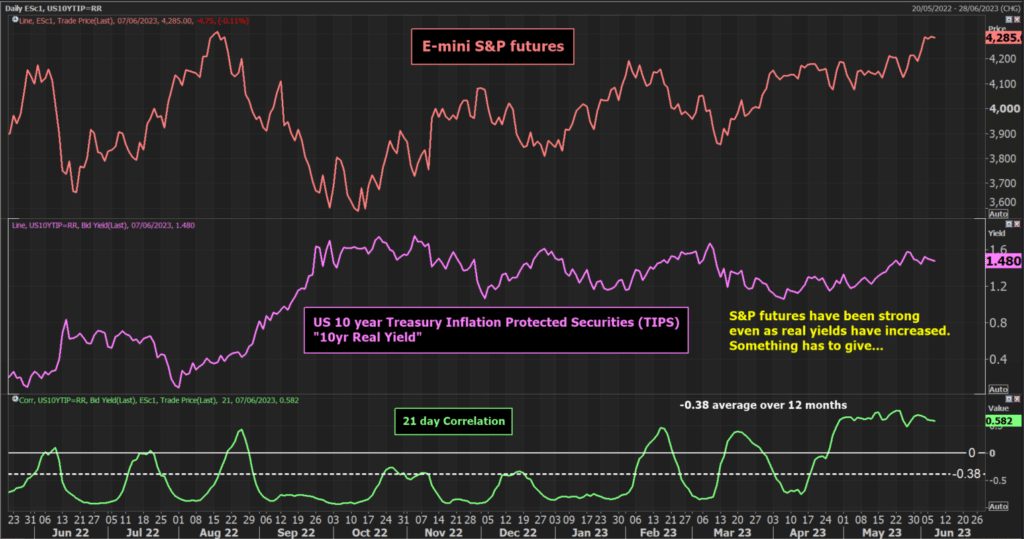

S&P 500 futures rallying despite higher yields

Historically, we see that US equities do not perform well during periods of rising bond yields. Higher interest rates tend to be negative for corporates. That has certainly tended to be the case, at least until recent weeks.

The e-mini S&P 500 futures have been sustaining a rally despite the rise in Treasury yields. The chart below shows the correlation between the S&P 500 futures and “real” US bond yields (measured by the US 10-year Treasury Inflation-Protected Securities). Over the past year, the correlation has been consistently very negative, with the occasional swing to no correlation. It is never too long before the negative correlation re-establishes.

However, in the past month, the rally in equities has held strong despite the rise in yields. This has left the correlation positively configured for several weeks. This is an abnormal position and is historically unsustainable. Eventually, something will give.

I wrote yesterday in my gold analysis, about how real yields were close to a multi-month ceiling at 1.57%/1.75%, but the question is whether yields will start to come down. With the Fed set to skip a hike in June, perhaps until July, this could leave yields still up around these levels. So it may not be falling yields that drive the next move.

Worries over market breadth remain

The worry I have with this bull run on US equity markets is that it is so narrow. I have spoken previously about the lack of market breadth in the move, with falling Advance/Decline lines.

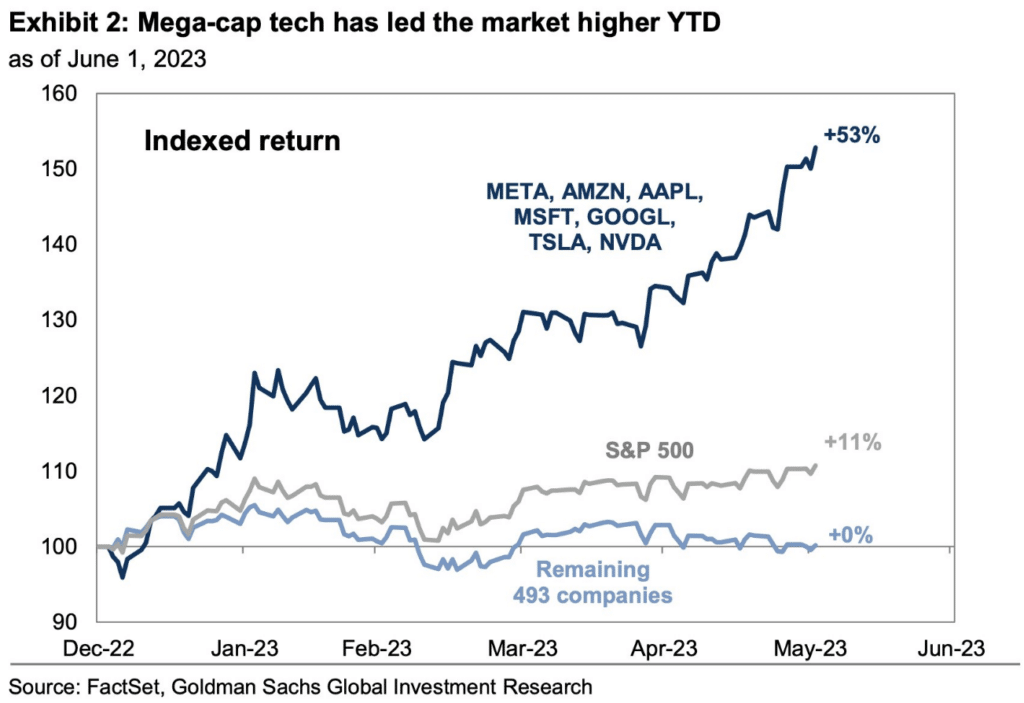

I then saw a chart this morning that caught my eye. It is from Goldman Sachs and it shows how just seven stocks are the primary reason behind the US rally. The mega-tech giants have been dragging Wall Street indices kicking and screaming higher.

As I said earlier, the S&P 500 futures were up 11% year to date. Without the mega-seven, it would be flat! For me, this does not smack of a healthy market.

The issue is that these tech stocks have been rallying hard and there is little reason to believe that they will not continue to do so. However, given the VIX is reaching levels of complacency (certainly compared to recent years), this sets up the potential for a corrective move.

Investors continue to climb a wall of worry on US equity markets, but it is a very narrow wall.