Macroeconomic/ geopolitical developments

- The Federal Reserve Open Market Committee (FOMC) met on Wednesday and as expected announced the start of tapering their monthly bond purchases by USD 15 billion later in November and December.

- However, the FOMC statement again highlighted an expectation for inflation to moderate and signalled no rush to tighten monetary policy.

- Markets viewed this as dovish, with stocks and Bonds both rallying.

- The Bank of England (BoE) met on Thursday and were widely expected to increase interest rates.

- But the lack of a rate hike and indication that rates are on hold for now added to the global Central Bank dovish tone from the Fed and European Central Bank (ECB) at recent meetings,

- Global Bonds moved to lower yields (rallying higher in price) and stock indices again advanced.

- The US October Jobs report on Friday showed 531K jobs added, beating consensus estimates, whilst the Unemployment rate fell to 4.6%. Again, this added to the “risk on” theme.

- Congress passed Biden’s $1.2 trillion social infrastructure bill at the weekend, which should further bolster the “risk on” view into this week.

Global financial market developments

- US stock averages led global markets higher with the S&P 500, DJIA and Nasdaq hitting new record levels to start November October.

- Global stock averages pushed higher into month-end, with the DAX at new all-time peak.

- US, UK and European yields rallied to multi-week yield lows after the recently more dovish ECB, FOMC and BoE meetings.

- The US Dollar has sustained a positive tone, despite the more dovish Fed.

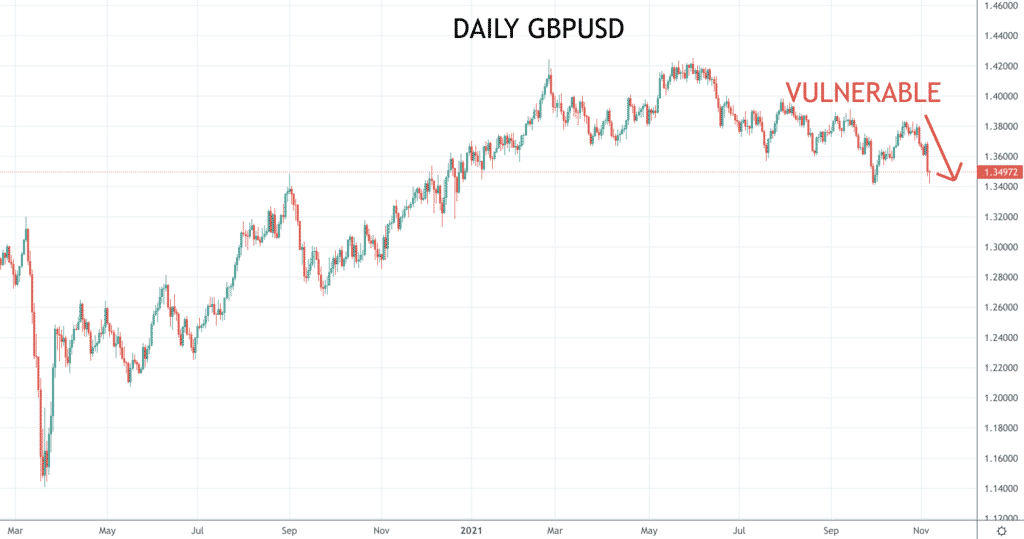

- EURUSD and GBPUSD have sold off with the US Dollar gains and with the dovish ECB, and BoE to sustain short- and intermediate-term vulnerability.

- losses late last week highlighted resurfacing weakness.

- Gold spiked higher to start November, with risk now for a more positive tone within a broader sideways range, maybe for a bullish range breakout.

- Oil sold off last week for a potential topping pattern.

- Copper losses retain a negative tone within a much broader range environment.

Key this week

- Geopolitics: Daylight Savings Time has ended in the US, clocks went forward. Thursday 11th November is the US Veterans Day holiday, US Bond markets are closed, stock markets are open.

- Central Bank Watch: A very quiet week for Central Banks with no activity of note.

- Macroeconomic data: The quiet data week too, the standouts are Chinese CPI, German and US CPI all on Wednesday.

| Date | Key Macroeconomic Events |

| 08/11/21 | Nothing of Note |

| 09/11/21 | German ZEW Survey; US PPI |

| 10/11/21 | Chinese CPI and PPI; German CPI; US CPI; |

| 11/11/21 | Australian Employment report; Veterans Day holiday, US Bond markets closed; UK Industrial & Manufacturing Production and GDP |

| 12/11/21 | Nothing of Note |