Macroeconomic/ geopolitical developments

- The standout event last week was the Fed Minutes which showed increasing talk of tapering Bond purchases later this year.

- The data even last week were the US Retail Sales numbers which fell 1.1% in July (though June data was revised higher).

- Chinese stocks remain under pressures with the ongoing regulatory clampdown on the tech sector.

- The continuing global spread of the Delta variant of COVID-19 keeps markets susceptible to sporadic, “risk off” moves.

Global financial market developments

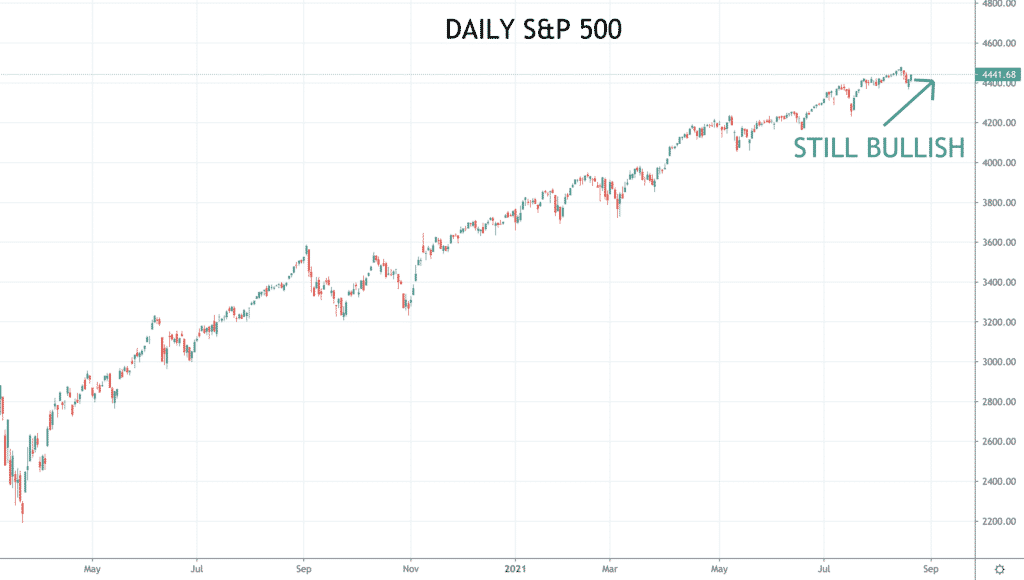

- Global stock averages rallied, fell and bounced last week, with Fed taper concerns driving the sell off.

- Despite the Fed taper talk, US bond markets prodded to lower yields.

- The US Dollar continues to strengthen

- EURUSD remains weak.

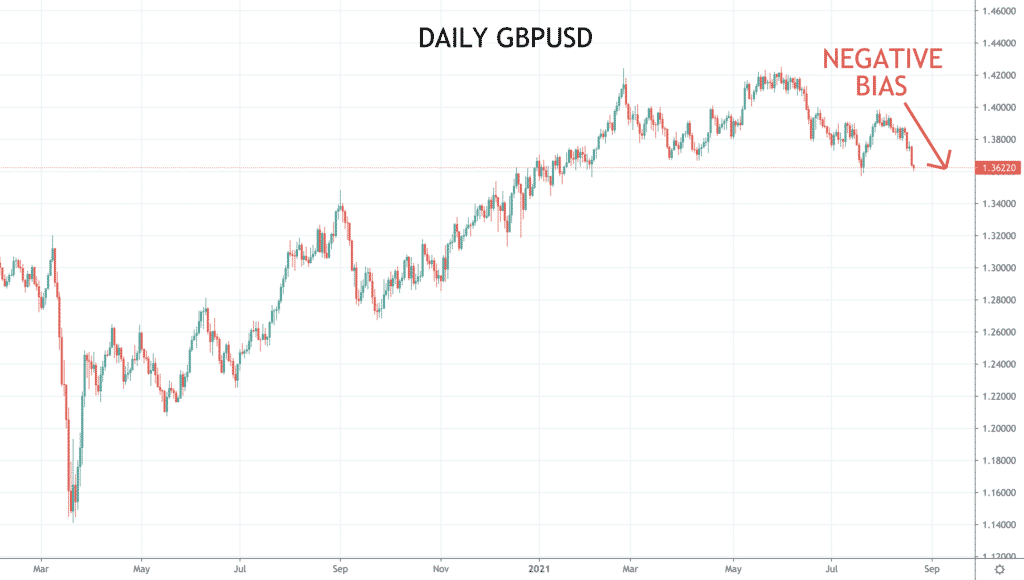

- GBPUSD looks vulnerable to further weakness.

- Gold remains vulnerable.

- The Oil price has plunged.

- Copper is weakening.

Key this week

- Geopolitics:

- Monitoring for a renewal of lockdowns or for further global lockdown easings.

- Watching the impact of the global spread of the COVID-19 Delta variant.

- Central Bank Watch: Little from central banks this week, BUT the Jackson Hole Economic Policy Symposium starts Thursday through to the weekend

- Macroeconomic data: Data standouts this week are the global Flash Purchasing Managers Index (PMI) data from Markit on Monday, German and US Gross Domestic Product (GDP) on Tuesday and Thursday respectively and German IFO on Wednesday.

| Date | Key Macroeconomic Events |

| 23/08/21 | Markit global Flash PMI; New Zealand Retail Sales |

| 24/08/21 | German GDP |

| 25/08/21 | German IFO; US Durable Goods |

| 26/08/21 | Jackson Hole Economic Policy Symposium; US GDP |

| 27/08/21 | Jackson Hole Economic Policy Symposium; Australian Retail Sales |