The ghastly problem with mantras about the economy, rules we think are certain, is that they only apply sometimes.

A useful macroeconomic trade is to play the FTSE100 to GBP, or pound sterling rate. This does only work one way though – FTSE rising does not change the value of the pound. But the GBP rate changing most certainly does change FTSE. Or, and here’s the problem, it should change it in a predictable manner but sometimes doesn’t. That’s the problem with mantras, these strict investing rules, sometimes they don’t work. Here the effect is strong enough that yes, it always does work. It’s just that an economy is a complicated enough thing that sometimes other things also happen. So, our thing which definitely does gets swamped by one of those something elses.

The idea here is that if the GBP rate rises then the FTSE100 should fall. The FTSE250 should fall a little bit less- in fact, about two thirds as much. Sadly for ease of trading it’s not the GBP/USD rate that matters, nor GBP/EUR. It’s not even the trade weighted rate either. It’s the rate at which London listed companies do business in those other currencies. Which is something not actually known – the trade weighted FX rate is the closest commonly calculated number to the one we desire.

This is not, though, on the basis that changing the FX rate changes trade. The BBC thinks it is but it isn’t: “The FTSE 100 stock index has closed at a record high, lifted by investors betting that a weak pound will help UK firms abroad” No, not right. Yes, trade does change with FX rates, but it takes a few years and usually (the “J-Curve”) goes the wrong way first before reverting. This is closer: “That is because the index on the London Stock Exchange has many firms with big footprints overseas. A weak pound makes goods they export cheaper for foreign buyers and helps inflate the value of business done elsewhere.“

Still not really right. The FTSE100 is not the 100 largest companies trading in the UK. It’s the 100 largest companies listed in London (and the FTSE250 is no 101 to 350). There are companies there (Antofagasta, say) which does not trade at all in the UK. There are others (say, Admiral) which are near entirely trading in the UK. The balance is that about 75% of the revenue to the FTSE100 comes from outside the UK. And is earned in currencies not GBP. But near all the companies report in GBP (OK, Unilever in EUR, oil in USD often, but…). So the FX rate for GBP is a big determinant of how big those foreign revenues and profits are going to be. It’s not so much trade that matters, it’s simply that the entire business is elsewhere and the profits flow back into sterling.

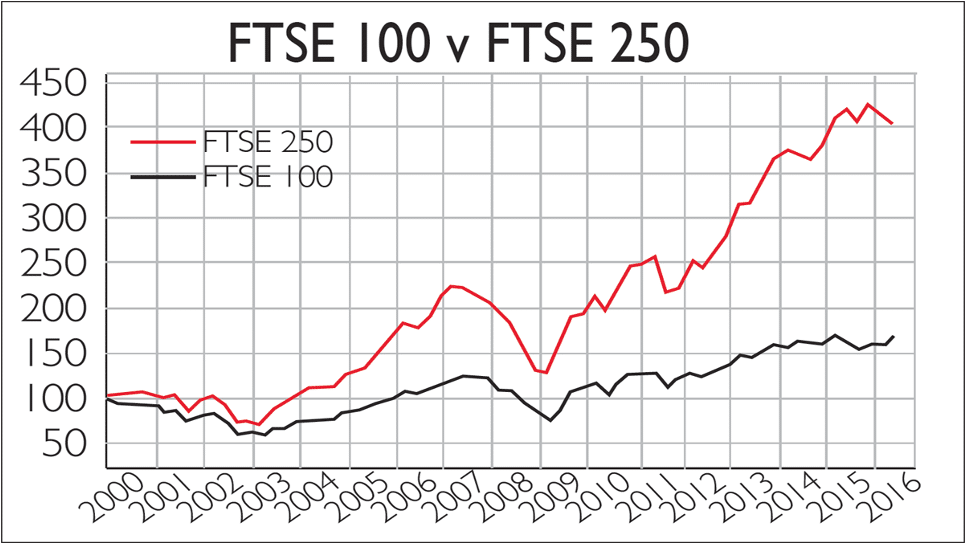

For the FTSE250 the rate is about 50%. Which is why the effect of GBP is lesser here than on the FTSE100.

Just to make this wholly obvious. If GBP falls then that foreign cash translated into GBP is worth more. So, reported profits, in GBP, rise. Vice versa when sterling strengthens. FTSE100 rises when GBP falls, falls when GBP rises.

Now, as above, that’s not the only FX nor macroeconomic effect in the economy. If GBP falls because the government decides to do something terribly stupid then the effect on FTSE could be of the terribly stupid thing more than the FX rates. Or, less dramatically, a change in interest rates will change the FX rate (in the medium to long term the determinant – yes, determinant – of FX rates is the relative real interest rates) but that change in rates might be taken as affecting the economy more than it does the GBP rate. You see what is meant by other issues sometimes swamping this, even if this still happens?

The most obvious and clear example of this was in the run up to and shortly after the Brexit vote. No, leave aside the politics of that (and I used to work for Nigel Farage so I’ll not be unbiased about that either) and observe just the FTSE gyrations. As it looked more like leaving, and then more like leaving the Single Market as well as the EU, then sterling fell. Because if you change the terms of trade, have to pay tariffs and all that, that will change an FX rate. But FTSE used to rise when GBP fell – for the reasons above. It was all rather fun watching the headscratching as remainers tried to work out why the stock market was rising as Britain made its terms of trade worse. The point about this story is that it was a time when the relationship was so very clear. There were so few other issues affecting either or both prices.

Reality is that there is a very direct relationship between the GBP FX rate and the FTSE100 and FTSE250 indices. It’s even one that’s possible to trade. But it is necessary to get the direction of GBP right first – and that, of course, is the difficult bit.