Macroeconomic/ geopolitical developments

- US equities posted their worst week since early September 2024, with the S&P 500 down 3.1%, the Nasdaq falling 3.5%, and the Dow Jones losing 2.4%, as trade policy uncertainty, economic slowdown concerns weighed on investor sentiment.

- Markets remained volatile as escalating trade tensions, shifting U.S. tariff policies, and President Trump’s altered stance on Ukraine fueled uncertainty, heightening investor concerns over rising costs, diplomatic instability, and global economic risks.

- The latest US PMI data showed a slight slowdown in manufacturing activity alongside continued strength in the services sector, while globally, modest manufacturing expansion was offset by weaker services growth and rising economic uncertainties.

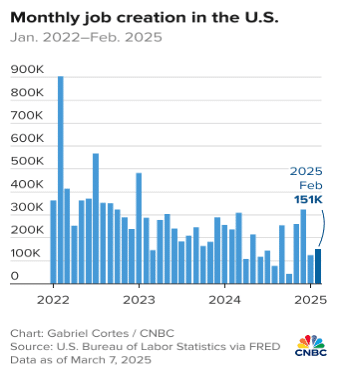

- The US economy added 151,000 jobs in February, slightly below expectations but above January’s revised figure, while the unemployment rate rose to 4.1%, with federal job cuts and trade uncertainty possibly weighing on future jobs growth.

- Investors and the Federal Reserve will closely watch February’s CPI report on Wednesday, which is expected to show core inflation rising 0.3% month-over-month and 3.2% year-over-year..

Global financial market developments

- US and global equity averages extended notably lower.

- US and more notably European bonds moved to higher yields.

- The US Dollar Index plunged significantly lower.

- Gold futures rallied, back close to its record high.

- Oil futures moved down to a multi-month low.

Key this week

Central Bank Watch: The main central bank activity this week is the Bank of Canada Interest Rate Decision and Monetary Policy Statement on Wednesday.

Macro Data Watch: The main macro data release this week is the US CPI data on Wednesday. Some other releases of note are the Chinese CPI data on Monday, UK GDP and US Michigan Consumer Sentiment Index on Friday.

US switches to daylight changing time: The USA switched to daylight savings time (DST) on March/9 2025. With European, UK and other countries not yet shifting to their DST as yet (for other countries that shift is mostly on the weekend of March 30 2025), this means that the time difference to the USA is currently narrower by one hour.

| Date | Major Macro Data |

| 03/10/2025 | Chinese CPI and PPI; EU Investor Confidence; German Industrial Production |

| 03/11/2025 | Japanese GDP; UK Retail Sales |

| 03/12/2025 | US CPI; BoC Interest Rate Decision and Monetary Policy Statement |

| 03/13/2025 | EU Industrial Production; US PPI |

| 03/14/2025 | German CPI; UK GDP and Industrial Production; US Michigan Consumer Sentiment Index |