Macroeconomic/ geopolitical developments

- The standout event in the week was Friday’s strong US Employment report, with 943K jobs added in June, notably above consensus estimates.

- Thursday saw the Bank of England Meeting and a slightly more hawkish tone stating that “some modest tightening of monetary policy over the forecast period is likely to be necessary”.

- Global PMI data earlier in the week was mixed, but with a notable beat for the US ISM Services PMI data.

- Slightly hawkish comments from Richard Clarida (Federal Reserve Vice Chair) and Christopher Waller (Federal Reserve Governor) added modest upward pressure on yields earlier in the week.

- The continuing spread globally of the COVID-19 Delta variant keeps markets vulnerable to intermittent, “risk off” moves.

Global financial market developments

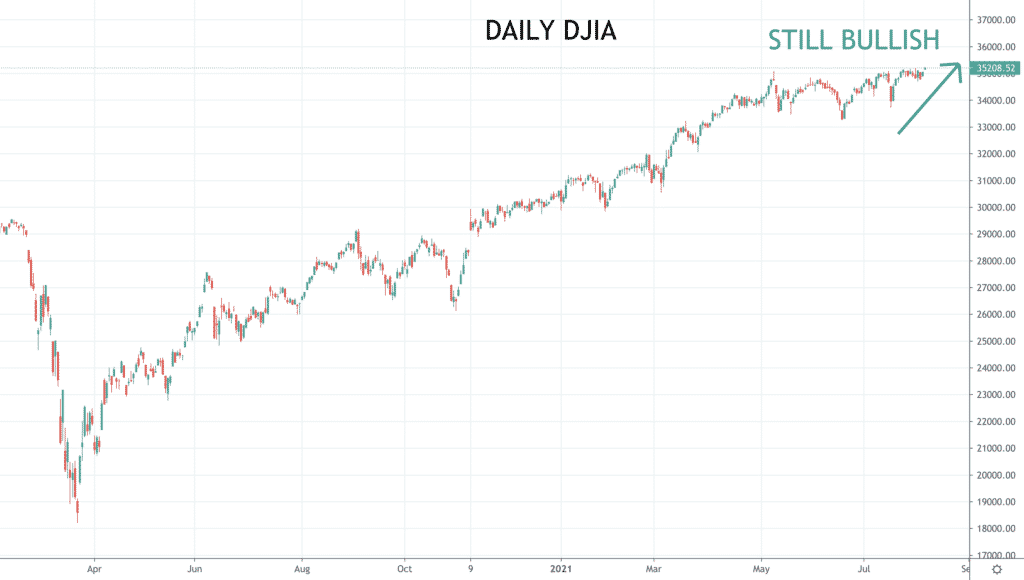

- Global stock averages marked time for much of last week but stayed firm before rallying Friday after the strong US Employment report.

- Global bond markets reversed some of the recent move to lower yields, after the strong US Employment report, with anticipation of possibly a move towards a more hawkish tone from the Fed and other major Central Banks.

- The higher US yields saw a broad US Dollar rally Friday and the US Dollar Index rebounded.

- EURUSD sold off Friday, submitting modest gains from early August, as the underlying bias remains negative.

- GBPUSD retreated slightly for a short time after the Bank of England on Thursday and further on Friday with wider US Dollar gains after the strong US Employment report.

- Gold saw a significant sell off Friday in thew wake of the broad US Dollar rally.

- The Oil price lost ground through the week and takes a negative bias into mid-August.

- Copper has sold off in early August and is aiming lower into this week.

Key this week

- Geopolitics:

- Monitoring the global spread of the COVID-19 Delta variant.

- Watching for further global lockdown easings.

- Central Bank Watch: We get the Reserve Bank of Australia (RBA) meeting minutes on Tuesday and the Reserve Bank of New Zealand (RBNZ) interest rate decision and statement is on Wednesday.

- Macroeconomic data: Data standouts this week are the global inflation reports through the week from the UK, EU, Canada and Japan, plus Retail Sales reports from China, the UK and US.

| Date | Key Macroeconomic Events |

| 09/08/21 | Japan GDP; China Industrial Production and Retail Sales |

| 10/08/21 | RBA meeting minutes; EU Employment change and GDP |

| 11/08/21 | RBNZ interest rate decision and statement; UK inflation data (including CPI); EU CPI; Canada CPI |

| 12/08/21 | Australian Employment report |

| 13/08/21 | Japan CPI; UK Retail Sales |