Selling pressure and elevated volatility have been crucial factors that investors have had to endure throughout a bruising year for financial markets in 2022. Anyone that has not been long of the US Dollar or has been unable to short the markets will likely be nursing some fairly hefty losses to their investing account.

However, coming towards the end of 2022, is this a good time to invest in financial markets? To answer this question, we consider the current market outlook and what could be set to come in 2023. Have markets hit the bottom and can a rally be sustainable?

What are the risks to investment today?

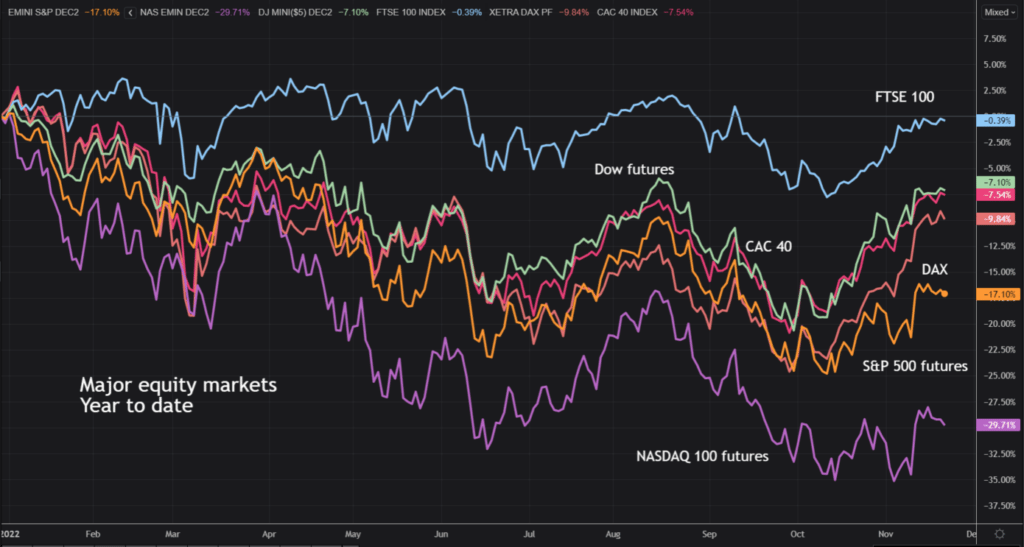

In 2022, we have seen bear markets (moves of over -20% down) for many major equity markets. Between January and October, the S&P 500 Index fell around -27%, whilst the NASDAQ 100 (i.e. “Big Tech”) had fallen by as much as -37% at one stage. Tech stocks have been smashed by the sharp tightening of interest rates. It has been a far more moderate decline for the FTSE 100 Index of less than -13%. The performance of the UK large-cap index has been helped by a heavy weighting in financials and energy stocks, whilst having minimal weighting in the tech sector. However, elsewhere in Europe, the German DAX Index, with its huge exposure to exports, has had a maximum drawdown of -27% this year.

Markets have already fallen a long way in 2022, but they could have further to go. There have been crucial factors behind the sell-off:

- Monetary policy tightening – major central banks around the world have engaged in a massive tightening of financial conditions. The ultra-loose monetary policy that fuelled the bull market moves since the recovery from the Great Financial Crisis of 2008 is being reversed. Huge inflation generated from the emergency pandemic response requires sharply higher interest rates. This has hit equity markets hard.

- The war in Ukraine – massive supply shocks, along with spiking prices for food and energy have come from war between Russia and Ukraine. This has plagued investors’ appetite for risk. There is little sign that the war will be ending any time soon.

However, these risks are still here. The era of low inflation is over for the perceivable future. Trends of anti-globalisation are running strong now as countries re-patriate production. Although the supply chain issues of the immediate wake of the pandemic are easing, there are still fears over the impact of China’s zero-COVID strategy. High inflation could prove to be sticky. Subsequently, the hawkish rhetoric amongst central banks remains prevalent.

The main risk to investing today is that markets continue to fall. Monetary policy tightening is ongoing. The Federal Reserve is still expected to raise the Fed Funds rate well into Q1 2023 (although this is likely to be the end of tightening). This means higher mortgage and living costs. The War in Ukraine shows no sign of easing, meaning the high cost of energy and food prices will significantly reduce the disposable income for consumers. High interest rates are negative for the outlook of equity markets.

Have markets bottomed?

Despite all this though, markets move on expectations. If the expectation is that, the Federal Reserve will soon pivot on its monetary policy tightening, this could prove to be a significant turning point for the expectations of investors.

We have already seen markets picking up significantly on the potential of a Fed pivot away from the aggressive hikes that have been seen during much of 2022. If there are less aggressive hikes coupled with potentially a lower “terminal rate” (the highest point of the interest rate cycle) on the horizon, then investors will move to price in a more encouraging environment for equities.

Here are a few reasons to believe that markets may have bottomed:

- Big downtrends have been broken on equity markets. European equity markets have recovered strongly to break their primary downtrends. US markets are lagging on this front, but that is mainly because of the big drag that the tech sector has had on the S&P 500 and especially the NASDAQ. Looking at the Dow Jones Industrial Average (much smaller tech presence) there is a strong recovery. The prospect for recovery is much greater following the decisive trend breaches.

- Reversal patterns are forming. Anyone that looks at technical analysis will see that the formation of reversal patterns on major indices is encouraging. Base patterns are an indication of a trend change. The question is how long-term the bases are. The recovery on the German DAX Index is far more decisive and better defined than it is on the FTSE 100 or S&P 500.

- The 2022 US Dollar (USD) positive trend has been broken. There has been a hugely strong and impressively defined USD bull trend throughout 2022. The USD has been almost the only major asset that has performed well during 2022. However, the USD strength has been one of the key indicators of the continued poor performance of higher-risk assets. The USD is seen as a safe haven investment and a go-to asset during market sell-offs. However, if the strong USD positive trend is being broken, it is a sign of a shift in sentiment for higher risk assets.

What is needed for a sustainable risk recovery?

For this to be a good time to be investing in financial markets, we need to see several factors decisively hitting inflexion points or already having turned the corner. Here are a few that we will be keeping an eye on in the coming weeks.

- Inflation sustainably tops out

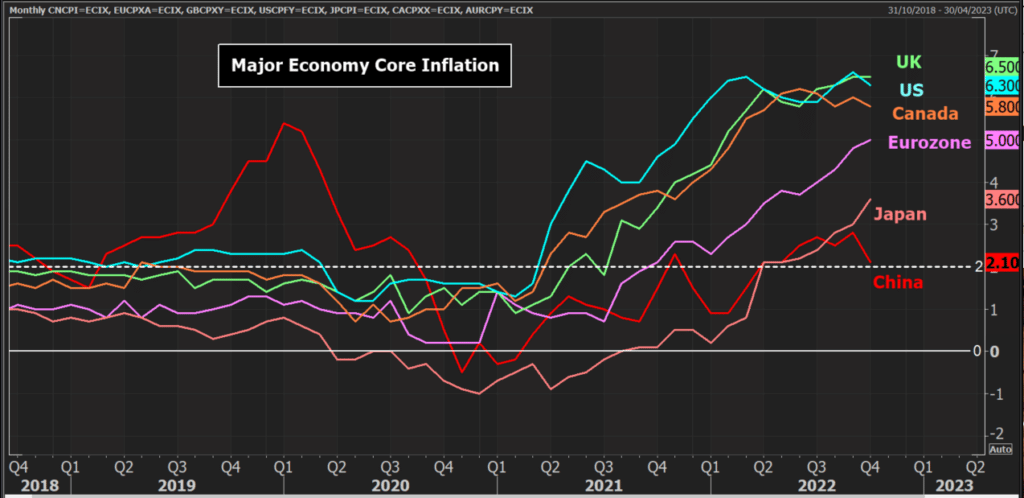

It is still very early, but there are signs that inflation has peaked in the US. The October US CPI reading showed a negative surprise. After several months of above-forecast CPI prints, there was a sharp drop in core CPI. Several Federal Reserve members have been quick to point out that this is just one data point and they would like to see a trend of months with inflation falling.

Looking at inflation data from the major economies, there are still rising rates in the Eurozone and Japan, whilst the US and UK are yet to show sustainable evidence of a peak. It will be a few months before we can be sure of a peak in inflation for major economies.

2. Real yields stop rising and start to decline

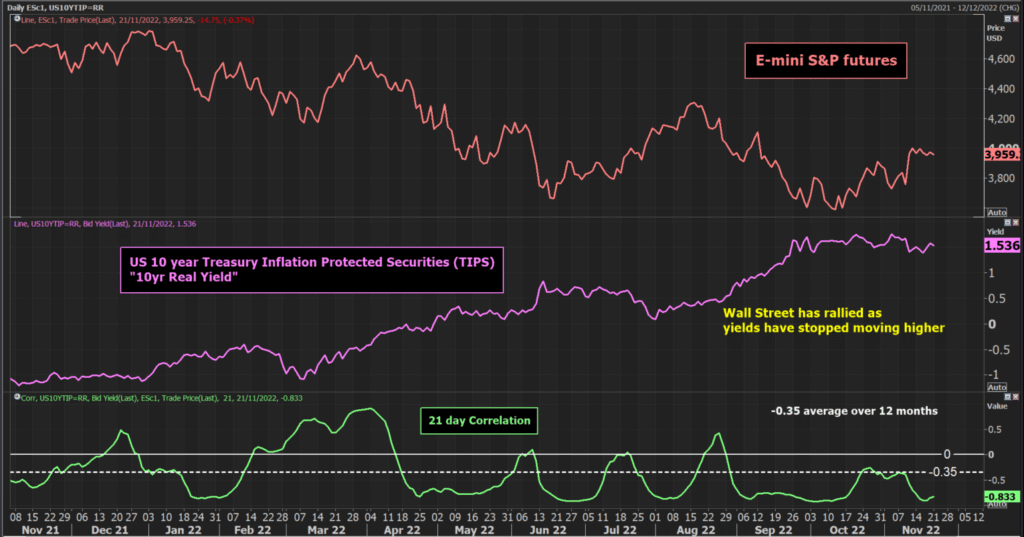

The sharp rise in bond yields has been a key factor behind the sell-off in risk assets in 2022. Real US bond yields (bond yields minus inflation) have a negative correlation to assets such as equities and metals. High and rising interest rates make it more expensive for corporates to borrow. Falling inflation is one thing for sentiment, but falling interest rates (bond yields) are a key factor too.

We have seen that real US bond yields have stopped rising in recent weeks. This has enabled a more positive outlook for equities. However, for a sustainable recovery to take hold, real yields need to start falling. We see in the chart below that there is a consistent negative correlation between the US 10-year real yield (measured by US 10-year Treasury Inflation-Protected Securities) and the S&P 500 Index futures. If real yields do fall back then the conditions would be much more favourable for a sustainable recovery in equities.

3. A USD rally needs to falter around 110 on Dollar Index.

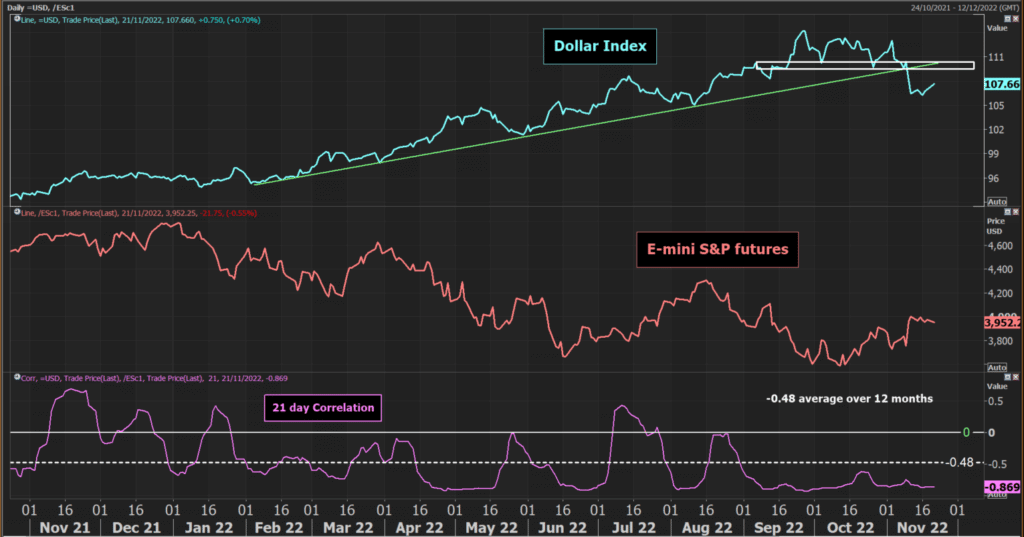

We have seen the big uptrend on the Dollar Index (DXY) broken. DXY has also completed a top pattern. The breakdown of the top now becomes a basis of resistance. If we now see technical rallies failing at lower levels then a sustainable correction on the USD can develop.

This is important as there is a negative correlation between the USD and equities. We can see in the chart of the Dollar Index and the S&P 500 Index futures there is a very strong negative correlation. Over the past 12 months, the negative correlation has averaged -0.48 which is extremely strong. A falling USD would set the conditions for a rally on Wall Street.

4. Support needs to form higher lows on any retracements

Improving technicals on the index charts needs to be confirmed. It is one thing for a market to rally, but there needs to be a confirmed test of resolve for the new trend. Therefore we would be looking for near-term corrections to be bought into. Higher lows are important in building a new positive trend.

Conclusion: Have stock markets bottomed? Probably

After months of sell-offs, bearishness, doom and gloom, there seems to be cause for optimism for investment as we approach the end of 2022. These green shoots still need to be confirmed and we have laid out a series of factors that we believe will help to achieve this.

In answering the question, “Should I invest today”, there is always a risk in any investment. The end of the Federal Reserve monetary policy tightening cycle is likely to come at some stage in Q1 2023. Markets are already preparing for this event. We do believe that given the forward-looking nature of financial markets, markets could be close to (or already in) the bottoming phase. It may still be a rocky road ahead, but we are far more confident about investing than at any stage throughout 2022.