UK economic growth is pretty anaemic. Headline inflation has only just dropped below double digits. Some would arguably point to the economy going through a period of stagflation. Despite this, the performance of GBP continues to stand up strongly against other major currencies. The Bank of England is having to prioritise inflation reduction in its monetary policy stance. Today’s labour market data shows that the BoE can afford to lean on the hawkish side over the coming months. This should help to sustain GBP performance.

- Unemployment is unexpectedly down, with wages higher than forecast

- This goes some way to justifying the significantly hawkish pricing for the Bank of England

- GBP performance remains strong on major forex

- Technicals show EUR/GBP and GBP/JPY are maintaining their recent trends

The UK labour market remains strong

This morning’s data from the ONS on the UK labour market was undoubtedly hawkish. Unemployment was expected to increase from 3.9% to 4.0%, the actual data showed the headline jobs rate fell back to 3.8%. If you delve into the detail there are some signs of the strength fraying slightly (for example, job vacancies are slightly lower). However, the total payrolled employees increased by 23,000 to 30 million in May (provisionally) versus an expected decline of 90,000. The inactivity rate continues to fall and the number of hours worked is increasing. Overall, the jobs picture still looks to be holding up very well given the sharp increase in interest rates.

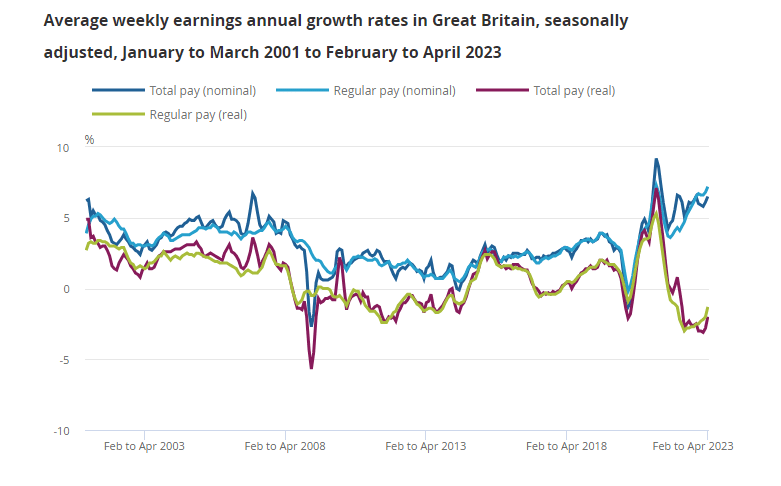

However, the headline grabber is that wage growth was much higher than expected in April. Regular pay increased to 7.2% (from 6.8%) whilst total pay (including bonuses) increased to 6.5% (from 6.1%). According to the consensus, both measures were expected to be around unchanged.

However, due to the high levels of inflation, real wages remain negative. Below is the chart of nominal and real wages from the ONS. Wage growth continues to track higher, whilst interestingly, real wages may finally be finding a floor and starting to improve.

The hawkish implications for the BoE

The continued strength of the jobs market is helping to fuel wage growth. It means that not only is the UK arguably facing stagnation, but the Bank of England also has strong wage pressures to consider too. I think that with real wages sitting around -2% and the trend of inflation starting to decline (admittedly though it remains very sticky), this does not come into the realm of a “wage/price spiral”. However, this is news that will be raising a few concerned eyebrows in Threadneedle Street.

Ever since the UK CPI inflation data came in much hotter than forex a few weeks ago, the pricing for Bank of England rate moves has soared. The current pricing for around 120 basis points of extra hikes will have little reason to be re-priced lower after today’s data.

However, ultimately as the year goes on, and inflation falls away, I find it difficult to fathom UK interest rates up over 5.5%. Rates are already restrictive in the UK. What I see is more likely is that, as with the US, the rate cuts will be pushed further out into 2024. Next week’s CPI inflation data will be keenly watched again.

This will sustain the move higher in GBP for now. However, there comes a point where this move will be fully priced in. Furthermore, markets may likely have to re-price for a lower peak rate as the year progresses. That could begin to restrict the upside in GBP.

GBP strength will sustain for the short to medium term

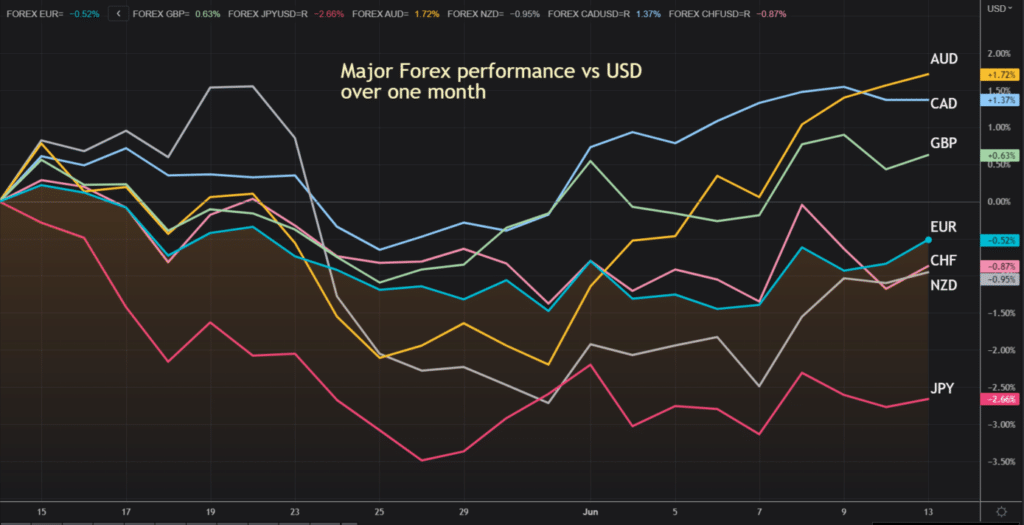

GBP has been strong for a while, holding up very well amidst the USD recovery of May and performing well against other major currencies. With interest rate differentials especially unfavourable for the Japanese yen, it is a consistent clear underperformer. We have also seen a continued lack of strength in the EUR too. The recent lower-than-expected May inflation is playing a role there.

However, the currencies of central banks that are posting hawkish surprises, the CAD and AUD are the consistent outperformers. With the upside surprises in CPI inflation and wages for April, GBP is not far behind. If UK CPI comes in hot once more in May, then this outperformance for GBP could continue.

GBP crosses remain sterling positive

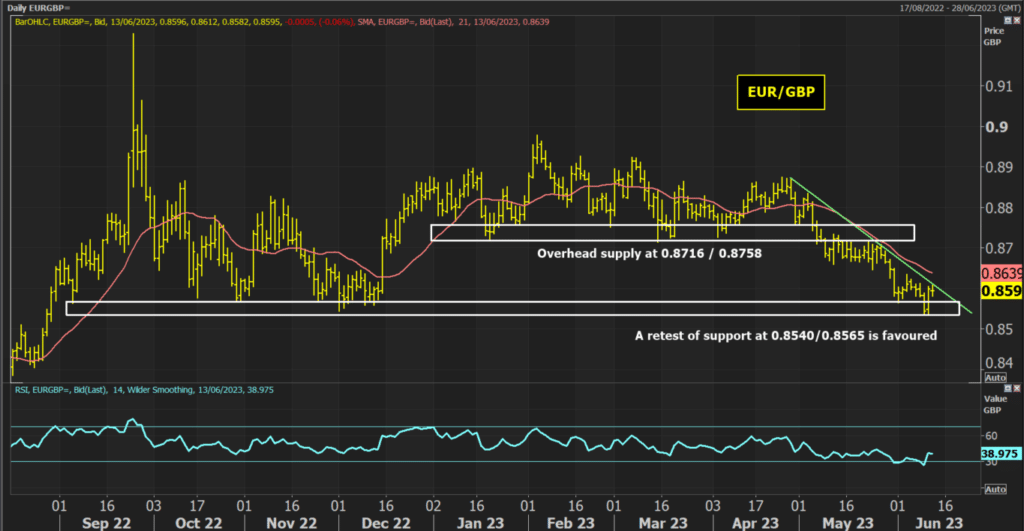

We are seeing notable strength in GBP on the crosses with EUR and JPY. Technical analysis shows some important trends are holding and key levels are being tested.

The downside move in EUR/GBP was jolted yesterday by a sharp rebound on the EUR. However, for now, this does not look to be an outlook-changing move. The UK data today also suggests this. A six week downtrend remains in place and rallies continue to be sold into. The daily Relative Strength Index shows that near-term rebounds struggle around the 40/45 area currently. Furthermore, the falling 21-day moving average is also a good basis of resistance now.

There is price resistance between 0.8636/0.8660 and if this restricts the rally then we expect a further retreat back towards a test of the key support band above 0.8540.

On GBP/JPY there is a big uptrend that has pulled the market higher for the past three months. The pair is trading at its higher since January 2016 and is showing minimal sign of looking for a reversal. Momentum remains very strong on the RSI without looking excessively overbought.

There is room for the odd near-term pullback within the trend. There is strong breakout support between 172.10/172.65, whilst the rising 21-day moving average is also an excellent near to medium-term basis of support. The longer-term chart suggests that the next basis of resistance is above 180.