Few people buy things that are unfashionable, that’s rather what it means. Therefore unfashionable things are cheap.

It’s one of those basic little rules – fashionable things are expensive because, well, they’re fashionable. Fashion itself just means that lots of people want it – so, simple supply and demand, lots wanting, the price goes up. This is also true of share prices. Sure, it shouldn’t be true because all investors are entirely rational types, right? But it is true – because humans worry about fashion even with money.

Two examples here are Imperial Brands (LON: IMB) and Legal & General (LON: LGEN). Because they’re unfashionable – although they’re unfashionable for different reasons – they seem cheap against objective valuations. The most important market of which is that their dividend yields are vast. If we looked just at those then we’d assume they’re immediate and nobrainer buys.

Of course, the divvie isn’t the only thing we should look at . There’s that thing called the “dividend trap”. Where a company is paying out so much in the dividend that it’s undermining its ability to keep going. There’s also the more technical thought that the share price might have dropped recently. The business is in trouble, the price drops, but the usual dividend calculations are on the past yield. Not the one that is going to be paid.

In fact, the possibilities of these are so high that when seeing a high divvie yield that should be our first thought. Not Wow, how cheap, but Blimey, what’s wrong? It’s only after we’ve ruled out something having gone wrong that we should think about a purchase in order to gain that yield.

These two companies, Imperial and L&G, pretty much pass those tests. At which point we’ve got to work out why the yield is so high – recall, we don’t expect to see high dividends so the existence is the thing that must be explained.

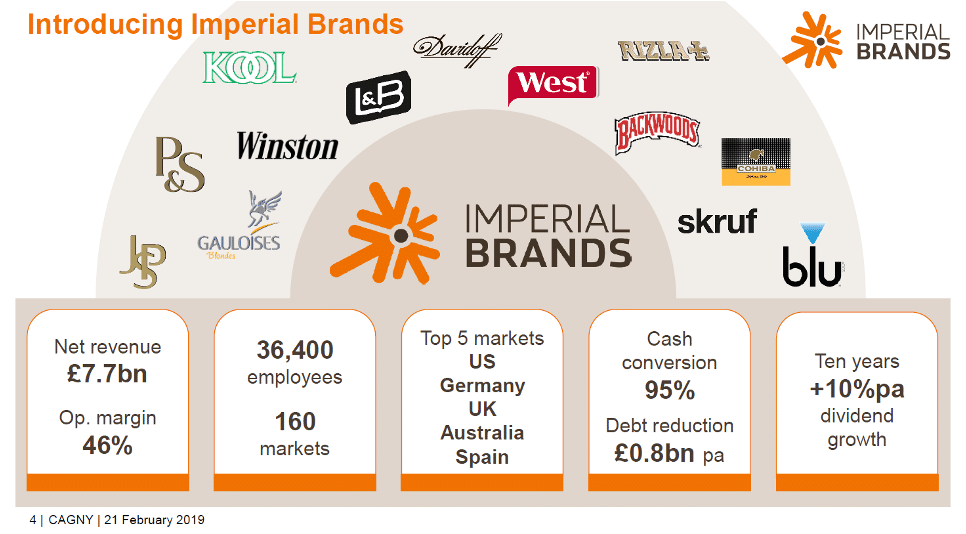

With Imperial this is easy – tobacco. ESG investing – that environmental, social and governance lark – is very anti-tobacco. It does, after all, kill many of those who indulge in it. So, that’s bad. That also means that the vast wall of money that is invested according to ESG principles does not go into tobacco stocks – of which Imperial is one. The ‘baccy business is also pretty stable, mature, makes good and reliable profits. So, the payout from those profits meets a low share price – a high yield. Imperial’s is 8%.

Share prices are not inflation protected, not formally they’re not, but they are pretty much. So that’s an 8% inflation protected (in reality, if not formally) yield – which is pretty juicy. We’re also unlikely to see much capital appreciation above any inflation related amount. Simply because the fashion isn’t going to turn. Not in any likely investment horizon it isn’t.

Legal and General now, that’s different. The yield is an even more juicy 9%. But financial services – the provision of pensions really – isn’t unfashionable in that ESG sense. So what’s going on here? The answer is necessarily a bit more hazy but it’s almost certainly the worries over that British pensions system. But L&G doesn’t fund pensions – which is where the problem is. L&G manages pensions, which is an entirely different game.

It is possible to think that L&G will be hit by rising interest rates. But we do seem to be near the peak of this interest rate cycle. So we should also – or could at least – think that L&G will benefit from the next turn, which is likely to be falling interest rates. Which gives us a slightly different view of the capital gains that might be possible here. For L&G seems to be cyclically out of fashion, not structurally so. Cycles change in fashions – heck some people are trying to bring bell bottoms and tank tops back – so it’s entirely possible that what is now out can be in again. This means that Legal and General isn’t just on the list of high dividend payers – it’s also possibly on the list for capital gains.

Which brings us to the real point to be made here. High dividends are great as long as they’re sustainable – avoiding that dividend trap. But even when we’ve identified that good income there are still those further questions to ask. Is this situation itself sustainable? If the out of fasihon going to remain so or is there the possibility of a capital gain as well?