Macroeconomic/ geopolitical developments

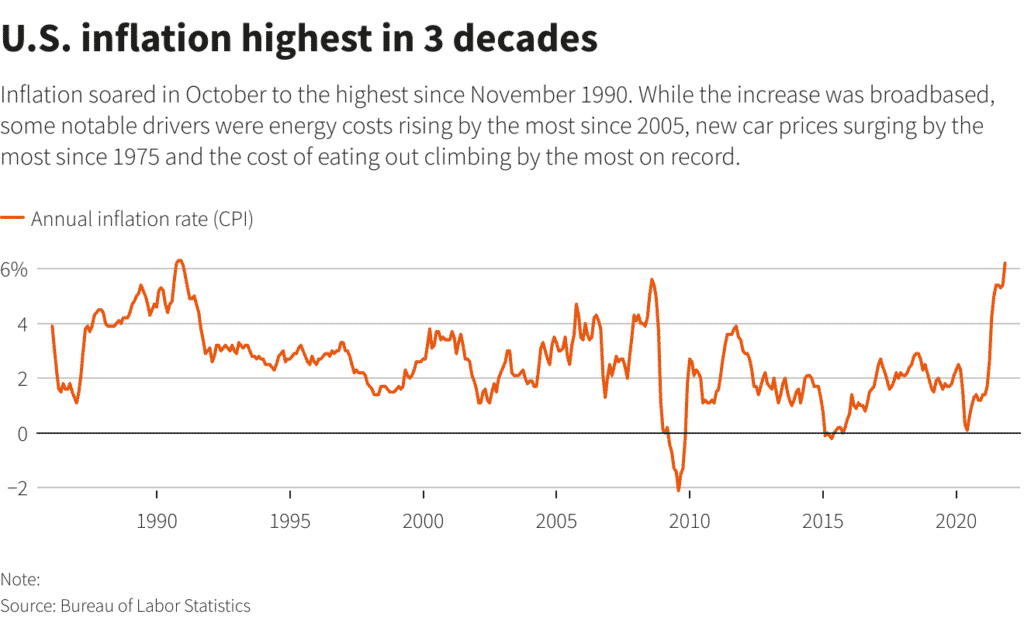

- The standout event last week was the US CPI data on Wednesday, which came in much higher than expected at 6.2% year-over-year, its highest level since 1990.

- This fuelled ongoing, underlying inflation concerns, seeing global stock indices setback (then bounce), whilst global bonds pushed to higher yields.

- Tesla saw a steep decline after CEO Elon Musk reacted to a Twitter poll and announced he plans to sell some of his shares.

- The Dutch government has ordered a partial lockdown to combat surging COVID-19 infections.

Global financial market developments

- US stock averages dipped from record levels from earlier November after the US CPI data release, whist European and UK indices stayed relatively strong.

- US, UK and European yields sold off to higher yields in reaction to the US inflation data.

- The US Dollar surged higher with the US Dollar Index hitting its highest level since July 2020.

- US Dollar gains saw EURUSD and GBPUSD further sell off, to sustain short- and intermediate-term vulnerability.

- Gold spiked even higher to start November, with risk now for a more bullish tone, maybe for a bullish range breakout.

- Erratic Oil price action last week, still a potential topping pattern.

- An erratic dip and bounce for Copper, but a negative tone within a broader range.

Key this week

- Central Bank Watch: A quiet week for Central Banks with the Reserve Bank of Australia (RBA) Meeting Minutes are released on Tuesday.

- Macroeconomic data: The standout data points are CPI data from the UK, Canada and the EU, Retail Sales data from China, the US, UK and Canada and the UK Employment report.

| Date | Key Macroeconomic Events |

| 15/11/21 | Japan GDP; China Retail Sales |

| 16/11/21 | RBA Meeting Minutes; UK Employment report; EU GDP; US Retail Sales |

| 17/11/21 | UK CPI; Canada CPI |

| 18/11/21 | EU CPI |

| 19/11/21 | UK Retail Sales; Canada Retail Sales |