In the wake of Hamas attacks, the US-brokered deal between Israel and Saudi Arabia now hangs by a thread. What’s going on?

In March 2020, when the covid-19 pandemic sent the UK into lockdown, half the country stopped work overnight. Not financial analysts though — as the global stock market lost a third of its value in the space of a month, most were making two predictions:

First, there would be a few months of frenzied activity, and second, that there was a good chance many of us would become surplus to business needs as the economy simply stopped.

Indeed, I distinctly remember telling my family that I would be working flat out for three months because I had no idea what my workload would look like thereafter. Of course, the markets recovered, and my career lived to fight another day.

And far from not having enough work to do, the opposite has occurred. Every time I try to book a holiday there’s another volatility event — the GameStop saga, the Ukraine War, the Partygate scandal, the Pakistan crisis, the Truss mini-budget, the US election, the Capitol riots, the Myanmar coup, the crypto surge (then winter), the Afghanistan withdrawal, the inflation story, Credit Suisse, Silicon Valley Bank, the interest rates crisis, escalating Sino-US tensions…

The list is pretty much endless, and these are just the events from the top of my head. There are also the non-events that can become important: Monkeypox was a non-starter, but this bed bug problem could be different.

Accordingly, I operate in a state of constant professional paranoia — where there’s always something around the corner. The four key economic issues that I think could kick off the next crisis include the bond market meltdown, generic state debt levels, a possible Chinese invasion of Taiwan, and the collapse of the commercial real estate bubble (in China or globally).

Of course, as I worry about these problems, they can’t really be considered as potential black swans. Instead, the weekend’s Israel-Hamas news could be an actual black swan that sends inflation rising again — the entire world knows there are tensions there, but few expected hostilities to escalate as dramatically as they have.

While the situation is clearly different to Ukraine, I’m struck by the similarity. No analysts thought Russia would invade, and no analysts thought that the Hamas attack from Gaza was possible given the fortifications around the strip. And yet here we are — with Israel formally declaring war.

Now before I go further, a couple of points:

- The human death toll is high and will likely mount. This is a tragedy and investors should continue to remember the human cost.

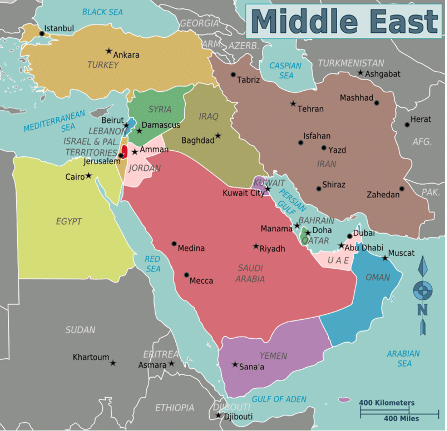

- Middle Eastern politics are beyond complicated. If you know what the following are, you might have 10% of the picture: Hamas, Intifada, Gaza Strip, West Bank, two-state solution, Hezbollah, Muslim Brotherhood, PKK, KRG, Shia, Sunni, ISIS, Al-Qaeda, Jihad, Fatah, PIJ, Houthi, Ansar Allah, Hadi, and Syrian Democratic Forces. If you can’t define even one of these, you have no chance.

What I’m not going to do is provide you with an insightful precis of the Six-Day War and Yom Kippur, or the various factions, alliances, and proxy wars going on. I spent several years at university doing this, and still know next to nothing — the politics are messy. The myriad religions, political factions, and states have been fighting in one form or another since at least the Crusades.

But there are some simple lessons which can be stated as fact rather than opinion. Here goes:

Where oil had its worst week in 17 months last week — Brent fell to less than $85 — this benchmark will likely now go above $100. And when oil goes up, so too will inflation, and this is particularly problematic as Europe has already lost access to Russian oil, and the US’s Strategic Petroleum Reserve is close to being tapped out.

But why will oil rise? To start with, it’s worth noting that the tensions and fighting could simmer down as they have in the past. But this is different — hundreds are dead (now on both sides, including children), and escalation now seems more likely than de-escalation.

In short, the Hamas group, which rules the Gaza Strip adjacent to Israel, has attacked its neighbour leaving hundreds of civilians dead. Israel has responded in kind.

Two members of Hamas and Hisbollah told the Wall Street Journal that the attack had been planned in meetings with the Islamic Revolutionary Guards Corps of Iran, since August — and the witnesses claim that the final go-ahead was given by Iran in Beirut last Monday.

Iran has long been accused of supporting jihadi groups in the Middle East, and its President Ebrahim Raisi has publicly announced that ‘the Zionist regime and its supporters are responsible for endangering the security of nations in the region, and they must be held accountable in this matter.’

Raisi has also urged the other Muslim governments to ‘support the Palestinian nation,’ while praising ‘resistance’ efforts by Hamas and Islamic Jihad not just in Israel, but also in Syria, Lebanon, and Iraq.

Now we get to the core of the problem. Over the past few years, the Middle East has come too close to a lasting peace. While this might not feel like a problem — it is to certain factions. Iran and the US recently agreed a prisoner swap including the release of $6 billion of frozen Iranian funds. And the two countries were also coming closer to a nuclear deal.

US Secretary of State Anthony Blinken thinks that a rapprochement (thawing of relations) between Israel and Saudi Arabia may have been behind the attacks — with the US behind efforts to bring the two nations closer. However, after the attacks, the Saudi foreign ministry has named Israel as ‘occupation forces’ and said Hamas acted as a ‘result of the continued occupation and deprivation of the Palestinian people of their legitimate rights.’

For context, Saudi is desperate to wean its economy off oil and diversify with the same success Israel has experienced. But it’s now effectively forced to back away from these ambitions to support Hamas, which governs the Gaza Strip.

Let’s rewind slightly. There are three key power players in the Middle East. Again, oversimplification, but:

- Israel, supported by the US and the rest of the western world

- Iran, supported by Russia and China, and which supports various destabilising factions

- Saudi Arabia, which plays all sides against each other to its own interests

During the Syrian War, Russia and Iran supported President Bashar al-Assad, while the west and Saudi Arabia supported various rebel groups. Meanwhile, the YPG and political wing SDF received support from the US to fight ISIS — annoying Turkey who views YPG as an extension of the banned PKK. Turkey was trying to stop the YPG from creating an autonomous state, while Israel tried to stop Iran from gaining influence using Hezbollah.

Simultaneously, Yemen is under continual conflict as the western and Saudi Arabia-backed government comes under attack from Iranian-backed Houthi rebels. And in the background, Egypt is still trying to recover from the 2014 military coup, Lebanon remains in economic crisis exacerbated by the August 2020 Beirut explosion, and Turkey continues to play everybody for power.

And that’s before you get started on Iraq — and Afghanistan, which we exited militarily from last year and is now controlled by the Taliban.

But the critical point to understand is this: to retain the current status quo, Saudi Arabia has to remain a neutral actor. It will support Russia and Iran by cutting oil production through OPEC, and fight Russia and Iran through proxy wars in Syria and Yemen. It will happily kill Jamal Khashoggi but work hard to be awarded the 2034 football world cup.

Turkey’s position is similar — it’s a bit simpler because the aim is to prevent YPG from getting a foothold in the Middle East. But at its core, Turkey is prepared to broker a grain deal between Russia and Ukraine, and support Putin in plenty of adventures abroad, but also acts as a key member of NATO. Europeans can generally understand Saudi’s position if likened to Turkey — both countries straddle two worlds and act accordingly.

Now to oil. As mentioned above, if oil rises, then inflation follows. If oil prices fall, then inflation falls. And before the weekend, it looked like a breakthrough was on the verge of happening.

The bones of the plan were that Saudi Arabia would formally recognise the state of Israel AND increase its oil production — in exchange for increased US military aid and increased political support.

Obviously, the US wants this, especially going into an election year — but Saudi also needs to diversify away from oil. This deal is essentially now scuppered because as a Muslim majority country, Saudi cannot agree a deal with a country (Israel) that is using advanced weaponry to kill Muslims.

Had the deal gone through, then Saudi Arabia would have tilted the balance of power towards the west — Iran, Russia and China would not have liked this — and arguably this is a core reason for the attacks.

Building on this, the tentative nuclear deal between the west and Iran may now break down, making increased oil output from the country unlikely as well. Iran has denied being behind the attacks — but has in the past also denied selling drones to Russia to fight in Ukraine.

Regardless of who was actually the mastermind, the trust is now gone. Most critically, had the Saudi-Israel deal gone through, Iran may well have decided to adjust to the new status quo by allying itself closer to the west — rather than continue wars where it would have become outnumbered.

And had Saudi agreed to increase oil production, then the rest of the OPEC cartel would likely have followed — and where supply rises, prices fall. Now it looks like oil will continue to remain high.

One final note. This is a very simplified version of events and should be taken accordingly. But going forward, it’s worth considering that while Saudi Arabia might need to publicly denounce Israel, they wanted a deal to go through and behind the scenes new efforts to make it happen will be ongoing.

But the problem is that the region is so volatile, that what starts as an attack can easily become an all-out war.

This article has been prepared for information purposes only by Charles Archer. It does not constitute advice, and no party accepts any liability for either accuracy or for investing decisions made using the information provided.

Further, it is not intended for distribution to, or use by, any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.