Of course, Lyft (NASDAQ: LYFT) and Uber (NYSE: UBER) has always been separate companies. But for much of their dual existence they’ve just been seen as two aspects of the same economic sector. If ride hailing and ride sharing work, then so will both companies – if they won’t then neither Uber nor Lyft will. It’s this which is changing, they’re each now seen and evaluated as being entirely different companies.

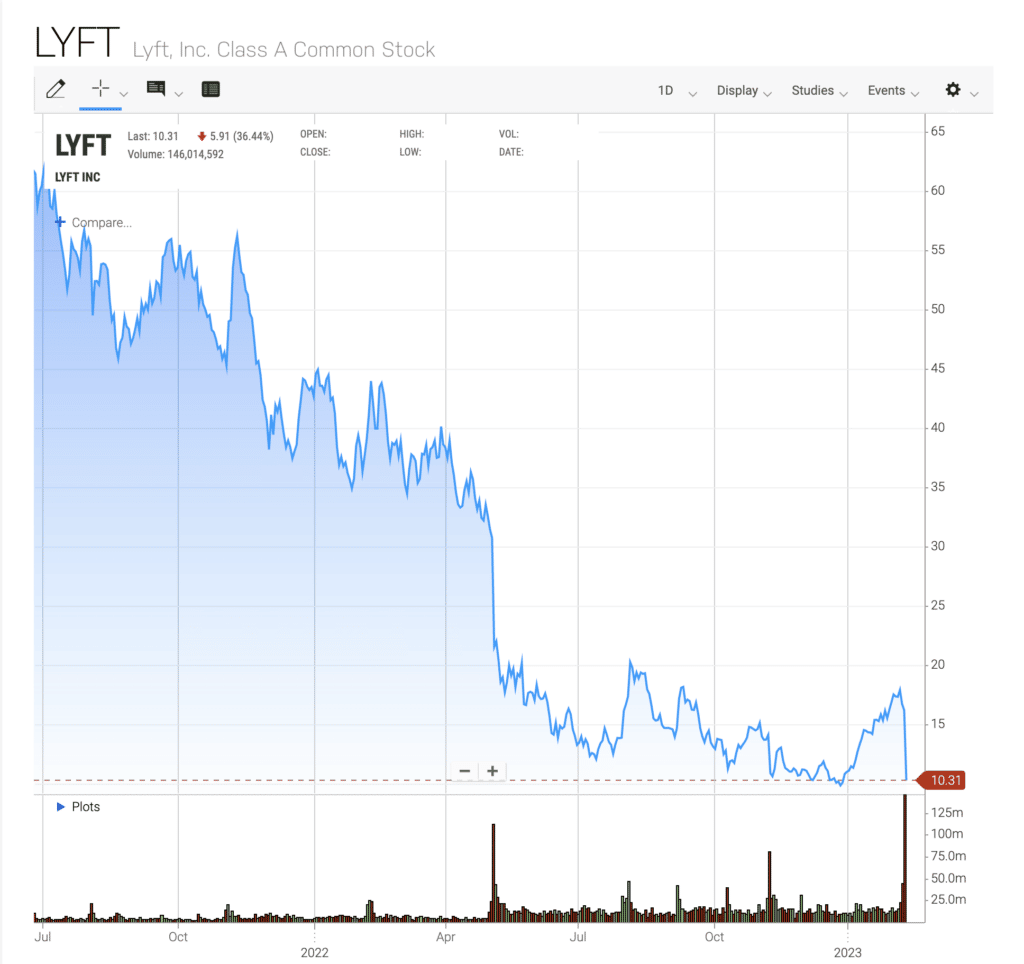

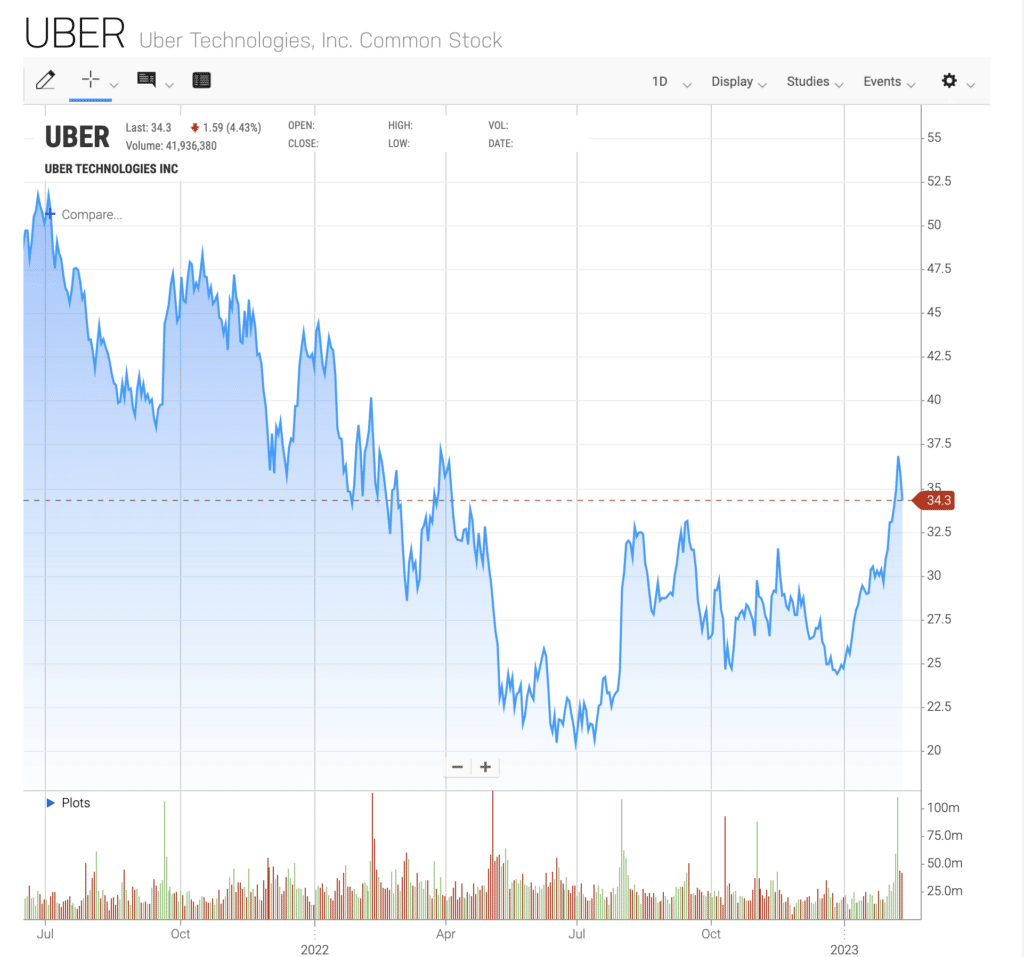

It’s this which allows Lyft to fall 36% in one day as the results are announced, Uber to only get hit 5% or so by the same news.

Or, perhaps more importantly, Lyft to be down 25% over the month preceding and including the latest news, Uber up 21% over that same time.

What Went Wrong at Lyft

The actual news itself is that Lyft is predicting a fall in revenues in this current quarter. A substantial one too, the prediction is for $975 million, some 10% down from analyst expectations, and a solid 20% down from the most recent reported quarter. That’s not good, of course. But the point here is a little subtle.

Lyft And Uber as a Sector, Not Businesses

Of course, businesses in the same sector will be affected by many of the same things. Laws against ride hailing would affect Lyft and Uber equally. Laws on how much drivers must be paid will have the same general effect and so on. That’s just like saying that both Shell and Exxon are affected by changes in the price of crude oil – well, yes, obviously. But we’ve a century of experience telling us that Shell and Exxon are differently affected even by obvious changes such as that of the price of crude. Which is the point being made about Uber and Lyft.

It really wasn’t that long ago – they’re both pretty new companies after all – that Uber and Lyft were seen as near duplicates. Anything that affected one of them would the other and in the same way. Their share prices reacted to that as well – the results of one were taken to be not just a guide but determinative of the results of the other.

Sector Valuation Methods

Now, it’s possible to take any valuation method a little too far. That old one about sell any company that builds a new HQ doesn’t always work for example – a new HQ can, even if only rarely, mean a strongly growing business. So too with this idea here. That Uber and Lyft are now entirely separate companies unaffected by mutual pressures. That would be to go that too, too, far. They’d both have horrible problems if the taxi unions gained more power for example. Not that we really tend to think that likely, it’s just that example.

The point is though that back only a few years no one knew whether the basic idea of ride hailing was going to work. Therefore, anyone trying it could – and possibly should – be evaluated on the same basis. Is this thing going to work or not?

Ride Hailing Does Work as an Idea

We now know that yes, ride hailing does work. Further, it doesn’t just work by cannibalising the taxi business. All the academic work one shows that it has distinctly expanded the market as a whole. Sure, some of the business enjoyed by Uber and or Lyft is a transfer of that old taxi trade. But more people are taking more rides as well – there’s been an expansion of the sector as a whole. Ride sharing/hailing does work by sating unmet demand and also seemingly creating more demand by making the service available.

OK, great – but that’s the very thing that gives us the differential evaluations. We are no longer valuing these two – and any other such companies – just on that one basis of whether the base idea is even going to work. We know that it does already. So, we no value each market sector participant by the skill and efficiency by which they operate.

In a Mature Sector Individual Performance Matters

Another way of putting this is that ride hailing is now all grown up. Therefore, the valuation of the corporations that do it depends upon the skill with which they exploit that market. Not, as before, on hopeful ideas about how large the market might be if it even works.

The effect of this is that we should, must even, be looking at Lyft and Uber as entirely different propositions. It’s no longer the basic market idea that matters – instead, it’s the quality of the management in exploiting it.