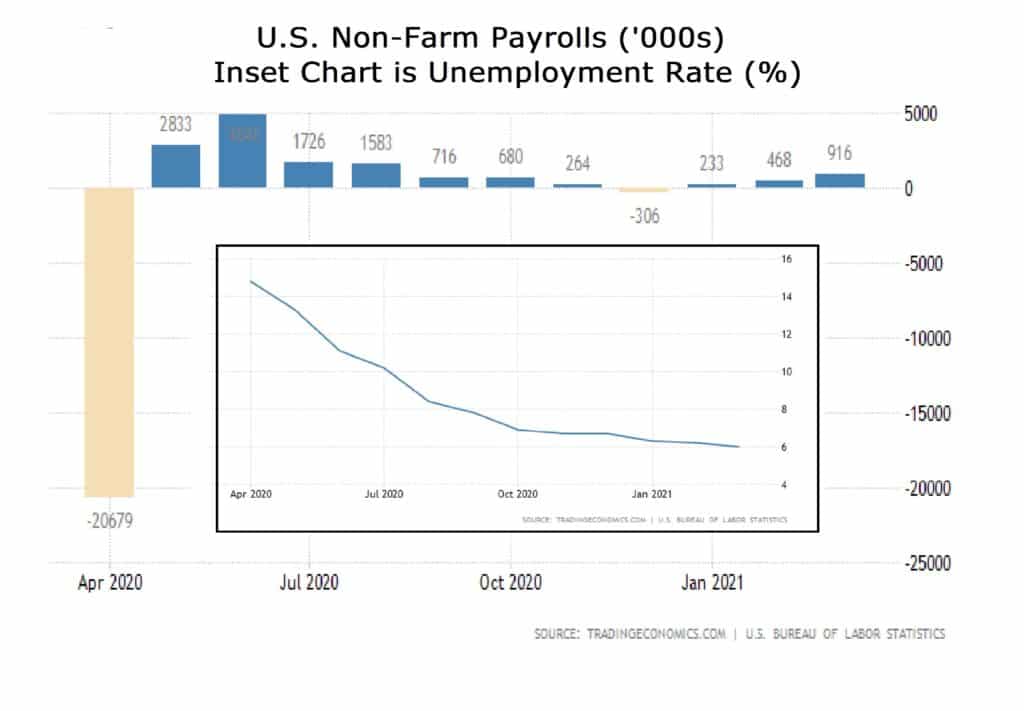

- Non-Farm Payrolls booked the best gain in seven-months

- The contrast in vaccine strategy and stimulus spending between the U.S and Europe is striking

- The economic paths of the U.S. cf. Eurozone and Japan are diverging

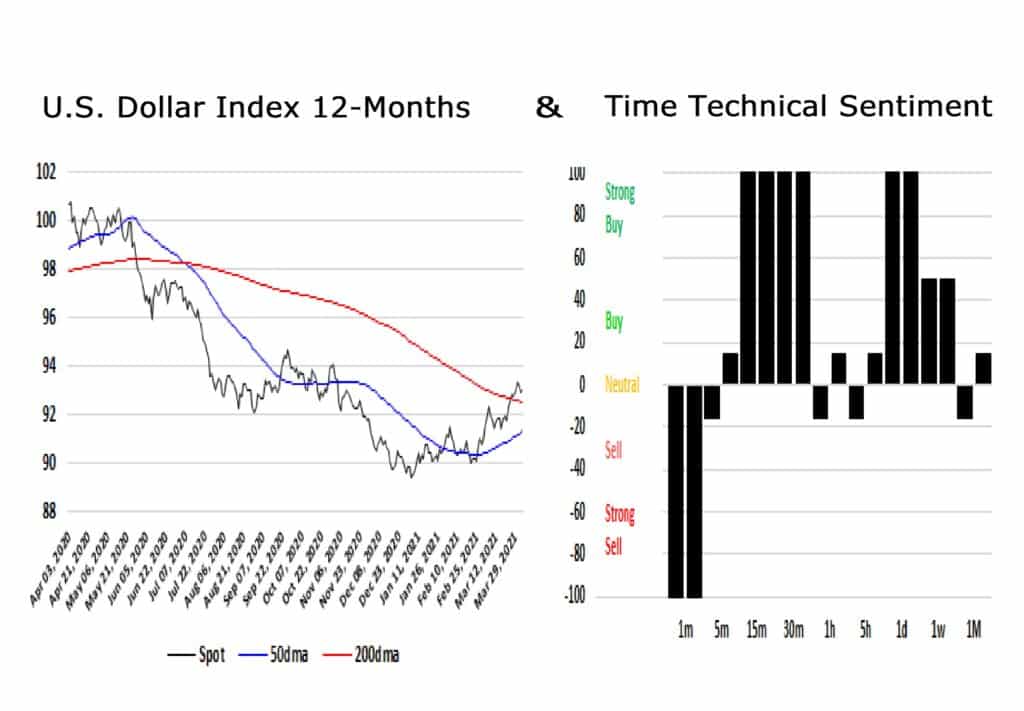

- The Dollar Index is set to rotate higher in an impulsive channel

It is an odd fact that Good Friday is not a U.S. government holiday. So even though many global markets, including U.S. equities were closed to enjoy the first day in the main Easter celebrations, the federal markets for Treasury securities and the Dollar were open.

The key data point of Good Friday was the U.S. Non-Farm Payroll figure that showed the economy added 916,000 jobs in March. This was the most in 7-months and was boosted by an upward revision to 468,000 in February.

As a result U.S. Treasury yields jumped…

T2 + 2.6 bps to 0.186% T5 +6.3 bps to 0.970%

T10 +3.5bps to 1.714% T30 +1.0 bp to 2.350%

… as it compared favourably to market expectations of 647,000, amid easing business restrictions, falling coronavirus infection rates, a fast vaccine rollout and continued support from the government.

Of course, one must look at these statistics in the round and recognise that the U.S. economy is still running at 8.4 million jobs shy of the peak in February of 2020 and so that shows just how severely the economy has been hit by the pandemic.

Still, we take glimmers of light where we find them and note that Fed Chair Jerome Powell recently said there was a good reason to expect job creation to accelerate up in the coming months even although it will take time to get back to the pre COVID-19 employment levels.

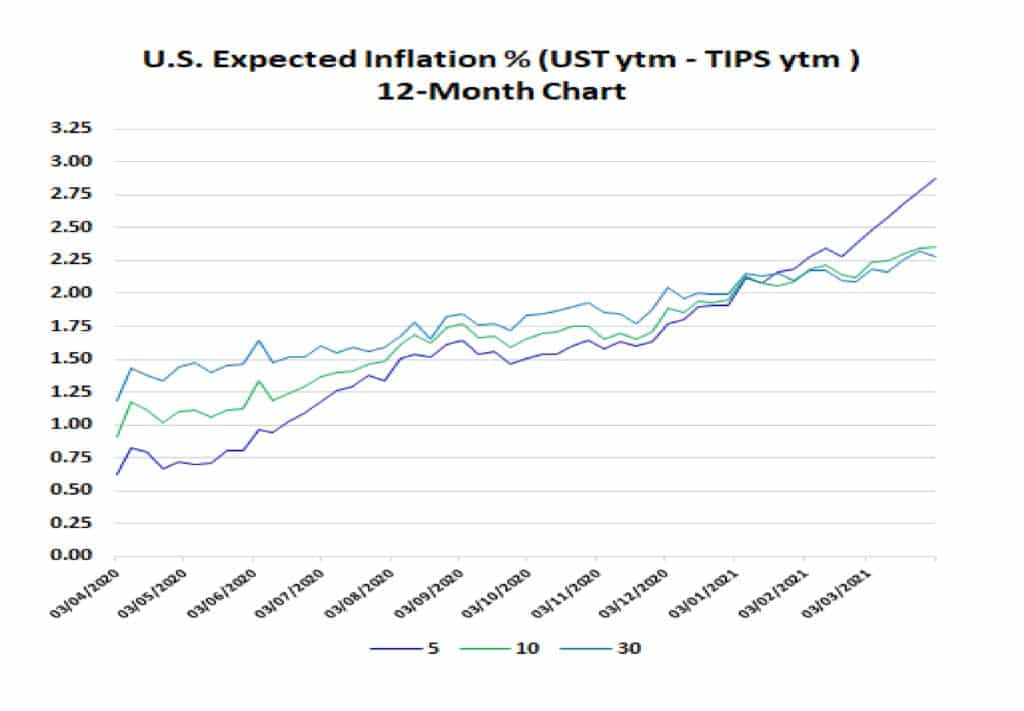

This data set is Dollar positive, for although we are still some way from a point when the Fed will pivot away from its low rate environment; the movement in inflation sentiment, Figure 2, does indicate an expectation of higher Fed Funds eventually coming down the track.

The Federal Reserve forecast average growth of 6.5% this year, up from 4.2% it predicted in December. Powell said he was not worried that weak growth abroad would hurt the U.S. which is, of course, the focus of the bank.

On that not we see in contrast, economists are cutting growth forecasts for the Eurozone economy as a third wave of COVID-19 infections and vaccination delays spur tighter restrictions in several countries including France, Italy and Germany.

Each month in lockdown will see 0.3 percentage points lost from Eurozone growth. The Eurozone will see its output gap run at double the equivalent differential in the U.S.. The takeaway from this is the European economy is creating fewer jobs, yielding weaker demand and generating lower inflation.

America will pull further ahead this year, while Europe is held back by less ambitious public spending, tighter restrictions on businesses and a slower rate of vaccinations.

If one looks at the 12-Month chart, shown below in Figure 3, one can see the spot price of the Dollar Index bottomed on January 5 at 89.409 and has since shown a pattern of rotation in an impulsive channel that has been in place throughout 2021 taking it through both key moving averages. The technical sentiment is a little mixed although with a slight bullish bias.

The World Beyond Europe

The Dollar Index must be seen against more than just the Euro and so it is fair to ask after the health of the Japanese economy. Economists are warning that the potential explosive spread of infections with variant strains of the novel coronavirus and a delay in vaccinations may put further downward pressure on the Japanese economy.

Japan’s consumer prices declined 0.4% year-on-year in February 2021, after falling 0.6% in the previous month, as the pandemic continued to weigh on consumption.

Although consumer spending will likely rebound in Q2, the pace of growth is expected to remain sluggish. A major fetter to growth is the lack of available vaccines. Japan’s vaccine approval process, which requires more clinical trials than many other countries, delayed the start date for vaccination. The proposed timeline for vaccination suggests that the general population will not even have access to vaccines until July.

The Price Path

The rotation trend we saw in Figure 3 is magnified in Figure 4 where one can see the Impulsive channel in greater detail. It now appears that the Dollar Index will rotate higher within the channel making a new local high at the 23.6% extension of the old range at 93.991.

I am a buyer of the Dollar Index as I see a more positive economic story emanating from the United States than in any other open market where I care to trade. I have a stop at 92.129 as a precaution, however, I target strength to the mid 94’s.