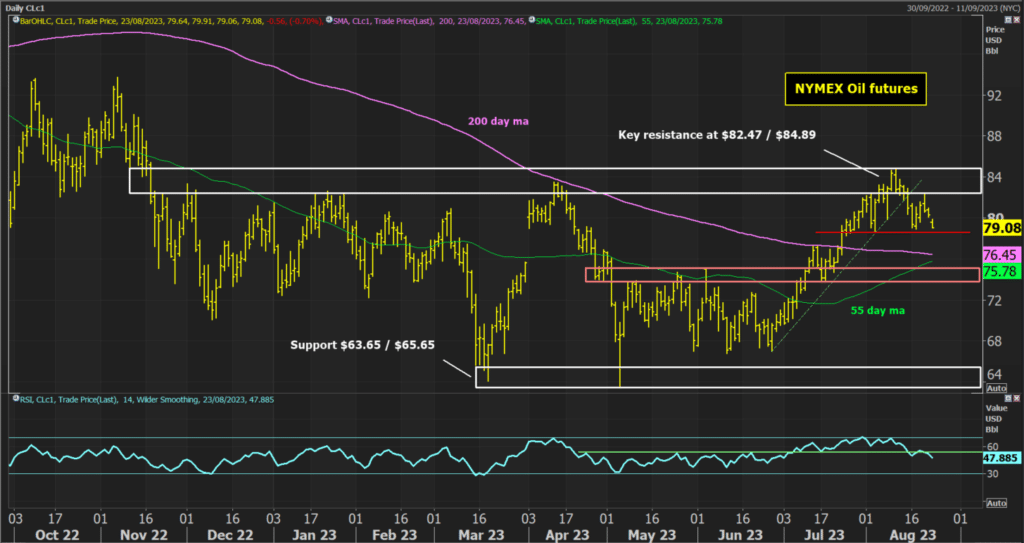

There has been a decisive recovery in oil futures since late June. A recovery that threatened to break decisively clear of key resistance and change the medium to longer-term outlook. However, the mood has shifted in the past couple of weeks, with futures going into retreat. This has come as there has been a shift in both the supply and demand dynamics of oil. This retreat is now threatening key support that if broken would complete a top that would signal a deeper correction.

- An economic slowdown in China is weighing on demand prospects

- Booming Iranian oil supply is damaging the efforts of OPEC+ to limit production levels

- Technicals show a top pattern threatens

Concerns over a Chinese economic slowdown weigh on oil

One of the key drivers of higher oil prices in recent weeks has been the expectation that Chinese authorities would be engaging in rounds of economic stimulus to pump up the faltering growth in the economy. However, in the past couple of weeks, there has been increasing concern over contagion within the shadow banking system amid the continued negative trends of the real estate market. There has been talk of stimulus by the Politburo, but no decisive or wide-ranging action yet. There have even been some suggestions that President Xi is looking to manage a slowdown of the Chinese economy.

This has resulted in cuts to expectations of Chinese GDP growth this year. Lower growth in China means lower oil demand. The positions that were taken by traders during the rally of July and early August may now need to be re-assessed. This reassessment of oil demand has weighed on the oil price, with NYMEX Oil Futures already having dropped over -6% from the August high of $84.89.

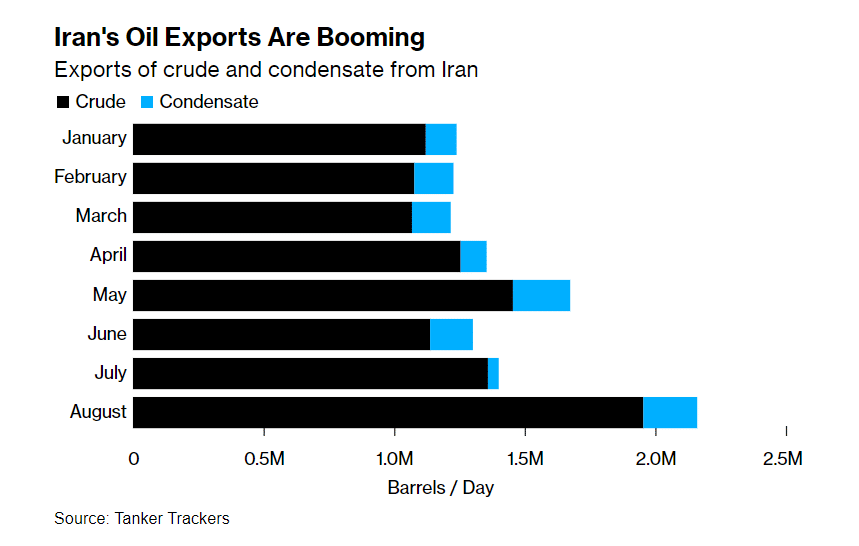

Iranian oil supply is surging

This change in the outlook for oil demand is also coming at the same time when the supply side of the equation has also been jolted. Recent data regarding oil exports from Iran would suggest that OPEC+ may not have the stranglehold on supply that it

Since the COVID pandemic, OPEC+ countries led by Saudi Arabia and Russia have been ensuring the global oil supply remains restricted. Production curbs have been controlled and even stepped up in recent months.

OPEC+ production fell month on month in July. The restricted supply of Saudi Arabia (with a voluntary production cut of 1m barrels per day) and Russia (cutting 500,000 barrels per day in August) has been a key driver of the rally in the oil price in recent weeks. However, it now transpires that these moves by OPEC+ are being countered by surging shipments of oil cargo by Iran.

Data from the shipping industry website TankerTrackers.com shows that in the first 20 days of August, Iran exported 2.206m barrels a day of crude and condensates. This is way above another other month of 2023 (the next highest was May with 1.719m barrels) whilst the average for 2023 is so far 1.362m barrels.

This data is changing the perception that OPEC+ are in control of the market supply. It is also contributing to the downside move seen in oil futures in recent sessions.

Technical analysis points to a correction

This decline in NYMEX Oil futures is also having a potentially decisive impact on the technical analysis too. With the retreat from $84.89, having broken the recovery uptrend, a new lower high formed this week at $82.47. This is now threatening to form a head and shoulders top reversal pattern.

The key support is at the old higher low of $78.69. A close below this “neckline” support would complete the pattern and imply a projected downside target of $72.49. This would suggest a correction back towards the mid-range pivot band at $73.84/$75.06 could easily be seen.

The formation of a new downtrend of lower highs and lower lows would put oil into a corrective near-term trend within what continues to be a nine-month trading band. The daily RSI has already broken to new seven-week lows and under 50 is leading the futures lower. This also suggests a new strategy of selling into strength for the retreat would be preferred. It just needs the closing break of $78.69 to confirm it.