Macroeconomic/ geopolitical developments

- Stocks faced a challenging week as tech-led losses weighed on the Nasdaq and S&P 500, global indexes mirrored declines, and rising Treasury yields added pressure, with the S&P 500 logging a 1% October dip that ended its five-month win streak.

- Alphabet, Amazon, and Apple exceeded earnings expectations despite mixed outlooks, while Microsoft and Meta saw strong performance tempered by cautious guidance and rising costs, leading to varied investor reactions across tech giants.

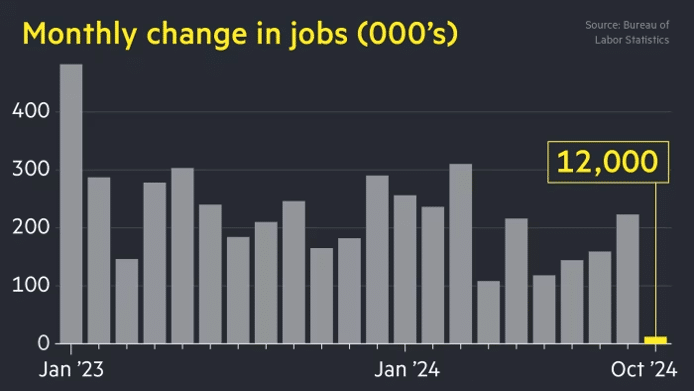

- The latest U.S. macro data revealed mixed signals, with inflation nearing the Fed’s 2% target while core prices remain elevated, and October’s weaker-than-expected job gains—due partly to strikes and hurricanes—supporting a cautious Fed stance on future rate cuts.

- This week’s U.S. presidential election and Federal Reserve meeting, which is expected to result in a quarter-point rate cut on Thursday, will likely raise market volatility, as investors closely watch for potential economic policy shifts and forward guidance from Fed Chair Jerome Powell amidst recent economic data.

Global financial market developments

- US and global equity averages dipped lower last week.

- US and European bond were higher in yield on the week

- The US Dollar Index marked time in consolidation mode, near multi-month highs.

- Gold futures pulled back late last week after hitting a new record level.

- Oil futures rebounded in a wider consolidation environment.

Key this week

Central Bank Watch: The main central bank activities this week is the Federal Reserve Interest Rate Decision and Monetary Policy Statement on Thursday. Some other activities of note are the Reverse Bank of Australia Interest Rate Decision and Monetary Policy Statement on Tuesday, Bank of Japan Monetary Policy Minutes on Wednesday and Bank of England Interest Rate Decision, Monetary Policy Statement and MPC Vote on Thursday.

Macro Data Watch: The main macro data release this week is the Global PMI date throughout the start of the week and US Factory Orders on Monday.

Geopolitics Watch: US Election – The US Presidential and Congressional Election is on Tuesday, with possible heightened volatility, although a result may take days or even weeks to be confirmed. US Daylight Savings Time ends – US Daylight Savings Time ended on the weekend of November 2nd/3rd. Global traders should be aware that opening, closing and data times could now be different in their local time.

See the macroeconomic data table on the next page.

| Date | Major Macro Data |

| 11/04/2024 | German and EU Manufacturing PMI; US Factory Orders |

| 11/05/2024 | US Presidential Election; UK Retail Sales; US and Chinese Service and Composite PMI; RBA Interest Rate Decision and Monetary Policy Statement |

| 11/06/2024 | BoJ Monetary Policy Minutes; German Factory Orders; German and EU Service and Composite PMI; EU PPI |

| 11/07/2024 | Chinese Trade Report; German Industrial Production; EU Retail Sales; BoE Interest Rate Decision, Monetary Policy Statement and MPC Vote; Fed Interest Rate Decision and Monetary Policy Statement |

| 11/08/2024 | Canadian Employment Report; Michigan Consumer Sentiment Index |