Macroeconomic/ geopolitical developments

- Poor results from US retailers, notably Target, but also Walmart, Lowe’s and Home Depot, highlighted a weakened US consumer.

- This stoked fears of a larger slowdown and future recession.

- This on top of US and global inflation worries, and hawkish Central Banks stoked the stagflation fire.

- Fed speakers, including Chair Powell have continued to send hawkish signals and highlight inflation concerns.

Global financial market developments

- The S&P 500 suffered its largest daily loss since June 2020 on Wednesday and on Friday the benchmark index entered bear market territory, down over 20% from its January record high.

- The late session, intraday rebound on Friday, however, avoided a more bearish signal and lends a slightly positive bias to the start of this week.

- European and UK indices have rebounded and are still outperforming their US counterparts.

- US 10yr yields broke even lower, with a safe haven bid.

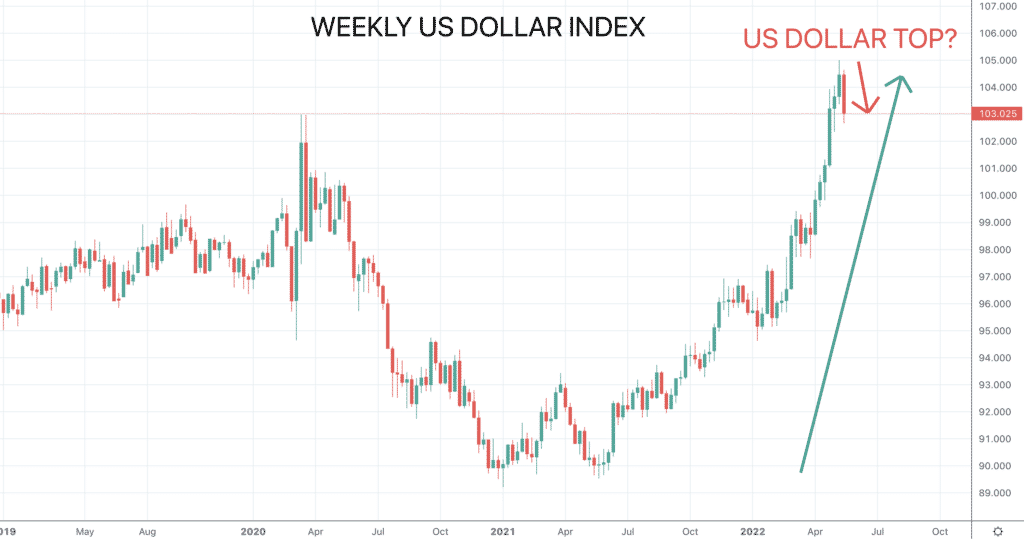

- The US Dollar weakened from its 2022 strength, as US yields moved lower.

- Gold rebounded with USD weakness, shifting to a more positive tone.

- Oil moved higher again, for a positive range theme.

- Copper bounced further to build a small base.

Key this week

- Geopolitical focus: Still closely monitoring the war in Ukraine

- Central Bank Watch: For Central Banks, the Bank of England (BoE) Governor Bailey speaks Monday, we get the Reserve Bank of New Zealand (RBNZ) interest rate decision, statement and press conference on Tuesday and the FOMC Meeting Minutes are released on Wednesday.

- Macroeconomic data: The standout data are the global S&P flash PMI data on Tuesday and US GDP and PCE data Thursday and Friday.

| Date | Key Macroeconomic Events |

| 23/05/22 | German IFO Survey; BoE’s Governor Bailey speech |

| 24/05/22 | Global S&P flash PMI data |

| 25/05/22 | RBNZ interest rate decision, statement and press conference; German GDP; US Durable Goods Orders; FOMC Meeting Minutes |

| 26/05/22 | US GDP and PCE; Canada Retail Sales |

| 27/05/22 | US PCE |