Macroeconomic/ geopolitical developments

- The European Central Bank (ECB) Forum on Central Banking 2022, from Sintra, Portugal saw the world’s major central bankers reaffirm their commitment to fighting inflation.

- The Manufacturing Purchasing Managers Index (PMI) data was mixed last week, with some of the European data beating expectations, whilst the US PMI data from S&P Global just beat forecasts, as the Institute of Supply Management (ISM) PMI data missed.

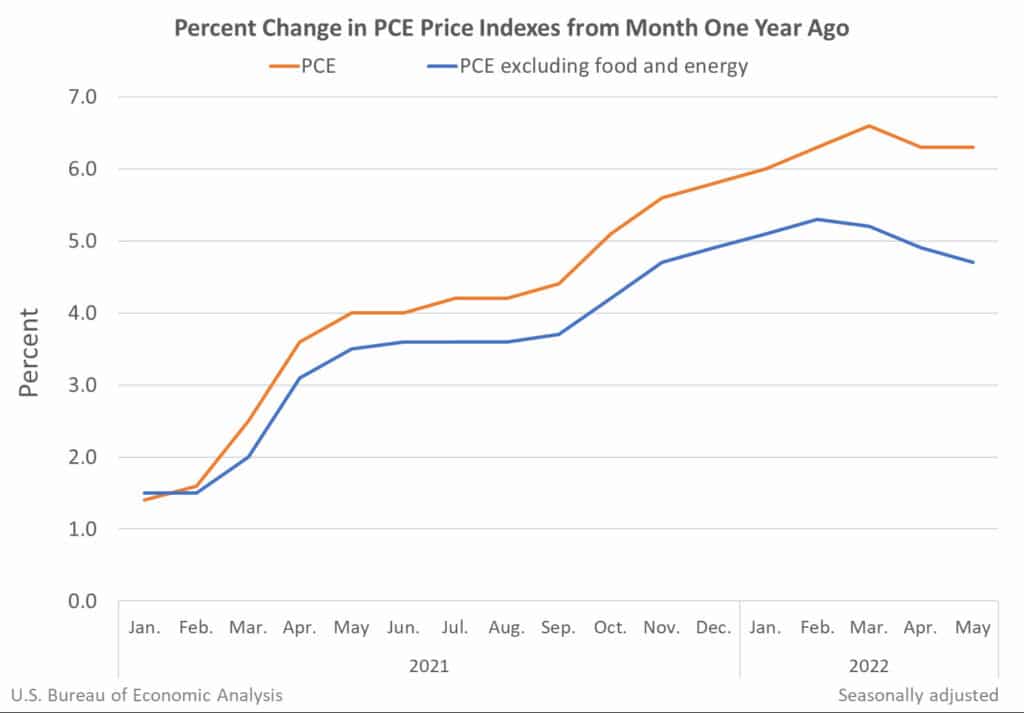

- The core (less food and energy) Personal Consumption Expenditure (PCE) data, the Fed’s preferred inflation measure, came in at 4.7% YoY for May, below expectations, the lowest level since November.

- Moderating inflation pressures but falling growth data saw global stock indices chopping in ranges, trying to build on gains and technical base efforts from the prior week.

Global financial market developments

- The major US stock averages were choppy and lower last week, but rebounded late in the week, still trying to build on the short-term bases hinted at the prior week as the S&P 500 moved out of bear market territory.

- European and Asian equity indices were mixed with European averages lower whilst Asian indices attempted to recover during erratic activity, still trying to send short-term bottoming signals.

- US 10yr yields moved even lower in yield back below 3.00%, to reinforce the lower yield activity from mid-June since the last US rate hike at the June FOMC Meeting.

- The US Dollar Index pushed back higher but remains capped by the June peak

- Gold sold off, threatening the recent base efforts.

- Oil was erratic, but the recovery failure has reinforced the mid-June short-term top and plunge, keeping risks lower.

- Copper plunged even lower to reinforce the prior break below the May low, to its lowest level since February 2021.

Key this week

- Geopolitical focus:

- Still monitoring the war in Ukraine.

- Monday 4th July is the Independence Day holiday in the US, markets are closed.

- Central Bank Watch: We get the Reserve Bank of Australia (RBA) interest rate decision on Tuesday and the release of the FOMC Meeting Minutes on Wednesday.

- Macroeconomic data: A busy week on the data front, we get global S&P Services and Composite PMI data on Tuesday, then Wednesday brings US S&P Services and Composite PMI, plus US ISM Services PMI, then the US Employment Report is released on Friday.

| Date | Key Macroeconomic Events |

| 04/07/22 | Independence Day holiday in the US, markets closed |

| 05/07/22 | RBA interest rate decision; global S&P Services and Composite PMI |

| 06/07/22 | EU Retail Sales; US S&P Services and Composite PMI and US ISM Services PMI; FOMC Meeting Minutes |

| 07/07/22 | US ADP Employment Change |

| 08/07/22 | US Employment Report; Canadian Employment report |