Macroeconomic/ geopolitical developments

- US CPI data was higher than expectations, with the headline data posting at 5% year-on-year for May, at its fastest pace since August 2008, with the core rate at 3.8%, its highest for nearly three decades.

- But Bond markets and stock indices shrugged off this data, with moves to lower yields and higher share prices respectively.

- On Thursday the ECB did not signal when it aims to begin lessening the stimulus program in response to the COVID-19 pandemic.

- ECB President Lagarde also stated “Headline inflation is expected to remain below our aim over the projection horizon”.

Global financial market developments

- Global stock averages pushed higher last week with the S&P 500 and the DAX positing new record levels

- Big Tech continued to rebound.

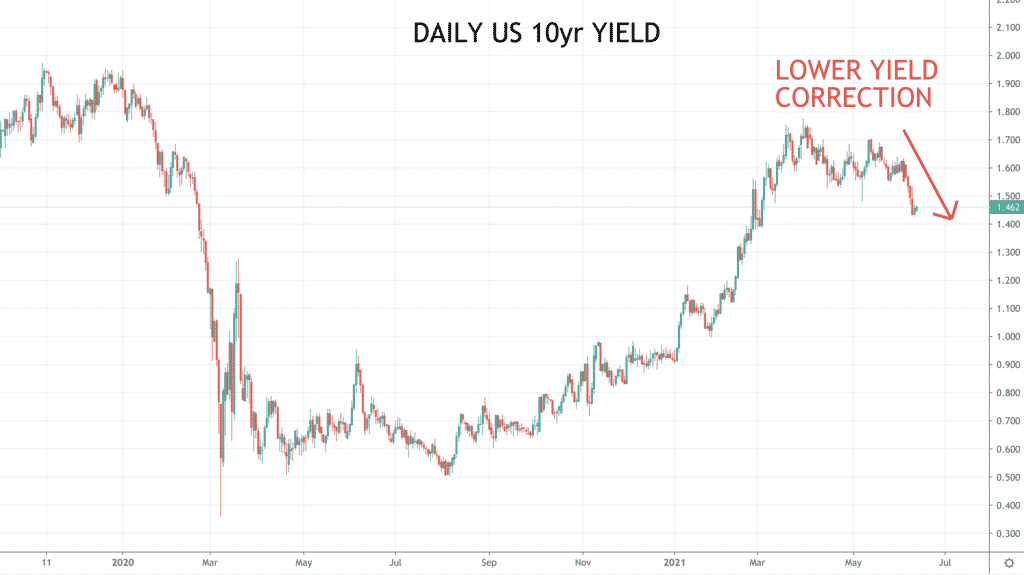

- US 10yr (and global) yields moved lower, despite the high US CPI data.

- The US Dollar Index rebounded gain from above key support, though lost ground on Friday.

- EURUS and GBPUSD have reinforced =topping patters having been capped below key resistance.

- Gold pushed lower, increasing topping threat

- Oil has extended even higher.

- Copper was sideways, again highlighting a topping threat.

- Global stock averages pushed higher last week with the S&P 500 and the DAX positing new record levels

- Big Tech continued to rebound.

- US 10yr (and global) yields moved lower, despite the high US CPI data.

- The US Dollar Index rebounded gain from above key support, though lost ground on Friday.

- EURUS and GBPUSD have reinforced =topping patters having been capped below key resistance.

- Gold pushed lower, increasing topping threat

- Oil has extended even higher.

- Copper was sideways, again highlighting a topping threat.

Key this week

- Geopolitics:

- Still looking for further easings of lockdown measures, particularly in Europe.

- Monitoring COVID-19 cases, hospitalisations and deaths globally, alongside the spread of the Delta variant in the UK and Europe.

- Central Bank Watch: We get the US Federal Open Market Committee (FOMC) interest rate decision and statement on Wednesday and the Bank of Japan (BoJ) interest rate decision, statement and press conference on Friday.

- Macroeconomic data: Data standouts this week are UK employment and Retail Sales, German and EU CPI, US PPI and Retail Sales.

| Date | Key Macroeconomic Events |

| 14/06/21 | Japan Industrial Production |

| 15/06/21 | RBA Meeting Minutes; UK Employment report; German CPI; US PPI and Retail Sales |

| 16/06/21 | UK inflation report; Canada CPI; FOMC Meeting, statement and press conference |

| 17/06/21 | Australian Employment report; EU CPI |

| 18/06/21 | BoJ Meeting, statement and press conference; UK Retail Sales |