Macroeconomic/ geopolitical developments

- US stock markets declined for the week amid tariff tensions, with the Dow and Nasdaq losing 0.5% and the S&P 500 slipping 0.2%, while U.S. Treasury yields fell as weaker jobs data and shifting inflation expectations fueled safe-haven demand.

- Market volatility persists as investors assess the impact of U.S. tariffs on China, alongside delayed duties on Mexico and Canada, with concerns over inflation, economic growth, and tariffs as a negotiating tool keeping uncertainty high.

- The U.S. manufacturing sector returned to expansion for the first time since 2022, while the services sector saw slower growth in January.

- Alphabet and Amazon shares fell after their earnings reports revealed weaker-than-expected cloud revenue growth, raising investor concerns over rising AI-related expenditures and slowing returns on massive capital investments.

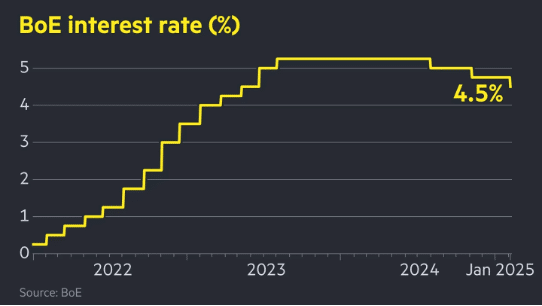

- The Bank of England lowered its benchmark interest rate to 4.5%, citing economic uncertainty and inflation risks, while signaling a cautious approach to further cuts.

- The U.S. labor market is gradually slowing, with January job gains falling short of expectations at 143,000, job openings dropping to a three-month low, and jobless claims rising, though wage growth remains strong, potentially delaying Fed rate cuts.

- Markets are closely watching Wednesday’s CPI release for signs of persistent inflation, as December’s 3.2% core inflation rate raised concerns among Fed officials, with a stronger-than-expected reading potentially delaying rate cuts.

Global financial market developments

- US and global equity averages dipped lower.

- US and European bond yields fell.

- The US Dollar Index spiked higher, then sold off.

- Gold futures rallied to another all time high

- Oil futures extended its grind lower.

Key this week

Central Bank Watch: Central bank activity is modest this week, with the key focus on Fed Chair Jerome Powell’s testimony before Congress on Tuesday and Wednesday.

Macro Data Watch: The main macro data release this week is the US CPI on Wednesday and US PPI on Thursday. Some other releases of note are the UK GDP on Thursday, EU GDP and US Retail Sales both on Friday.

| Date | Major Macro Data |

| 02/10/2025 | Nothing of note |

| 02/11/2025 | UK Retail Sales; Fed Chair Jerome Powell testifies before Congress |

| 02/12/2025 | US CPI; Fed Chair Jerome Powell testifies before Congress |

| 02/13/2025 | German CPI; UK GDP and Industrial Production; EU Industrial Production; US PPI |

| 02/14/2025 | EU GDP; US Retail Sales and Industrial Production |