As the coldest days of the Northern Hemisphere winter arrive one can expect energy stocks to receive fresh impetus as global investors seek positions that will derive economic benefit from expected increase in prices and the shortages expected.

In September, as autumn leaves were starting to fall, 66% of the respondents to a survey conducted by MLIV Pulse; it included both professional portfolio managers and retail investors, indicated that they were looking to increase exposure to the sector over the next six-months. Their driver for this action was they foresaw electricity and natural gas prices driving global inflation as the Russia and Ukraine war would persist well into 2023.

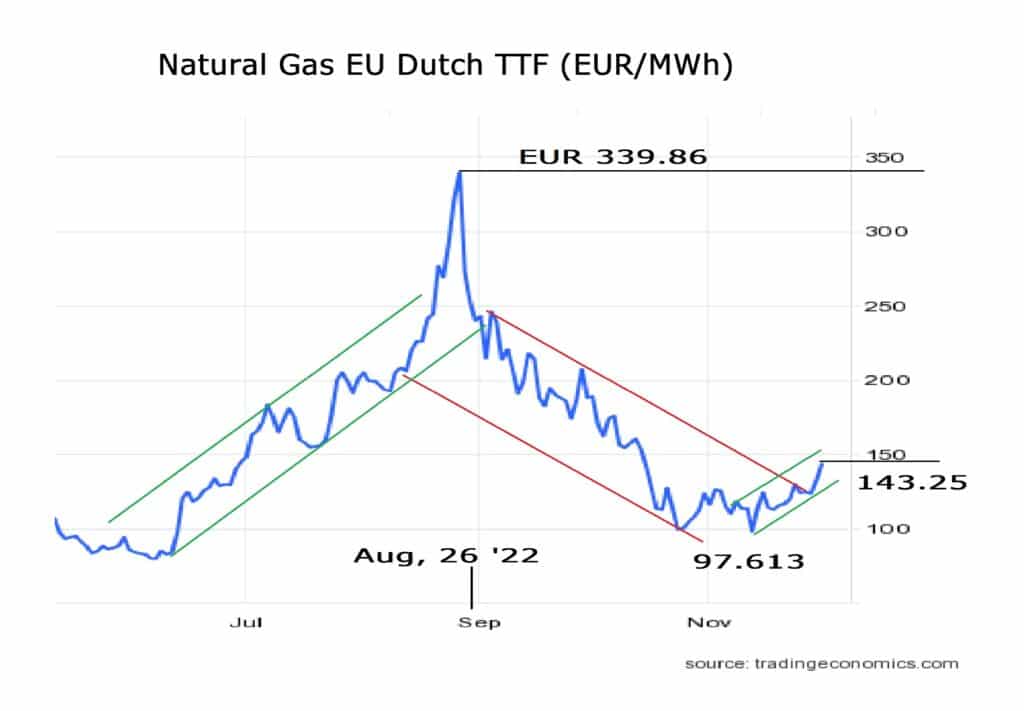

Dutch front-month natural gas futures are, of course lower than the high of EUR 339.86/MWh booked on August 26. However, on November 29 they rose for a second consecutive day to trade above EUR 135/MWh. That is the highest since October 14th acting as an extension of recent gains in November to 46.75%.

This was driven by forecast of freezing sub-zero weather starting next week across Europe that will see a draw down on inventories. It is a good job then that storage facilities in the EU were 93.9% full as of November 27th, with German facilities recording 98.9% of capacity.

The next test for this market is the 23.6% retracement of the 97.613 – 339.860 range that sits at EUR 154.783/MWh and then that at 38.2% at EUR 190.151/MWh. These targets are a real prospect as there are currently issues with processing at the Troll field in Norway and the Barrow North terminal in the UK. However, one must note that Gazprom continues to send gas to Europe via Ukraine and has said the company said it has decided against reducing supplies to Moldova, while reserving the right to lowering them or cut shipments if Moldova fails to meet pre-agreed payments.

Another positive driver is found inside the hub of EU politics as regional energy ministers agreed to postpone the approval of a proposed gas price cap at EUR275/MWh to mid-December.

Who is making money from energy crisis?

The answer to this is the entities that sell energy direct to consumers, although the major profits are being booked by the oil and gas producers.

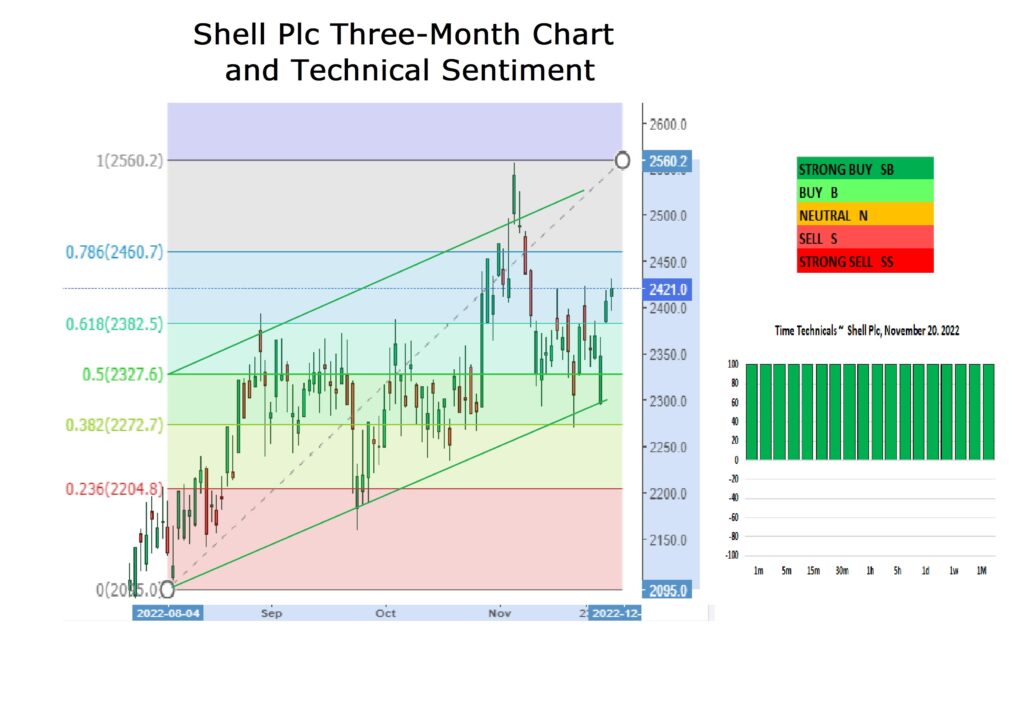

Shell Plc is a British multinational oil and gas company headquartered in London, England.

On October 27 Shell reported that it had strong Q3 2022 results at a time of ongoing volatility in global energy markets. The company was strengthening the investment portfolio to assist the transition for the low to zero carbon future, (see below). It was also collaborating with governments and customers to find workable solutions to their short and long-term energy needs.

Shell announced a new share buyback programme resulting in an additional USD4 Billion of distributions that should be completed by the Q4 2022 results announcement as well as increasing the dividend per share (DPS) for Q4 to be paid in March 2023, by an expected 15%, subject to approval.

On Monday, November 28 the company said it was to acquire Danish biogas producer Nature Energy for nearly USD2 Billion, as it looks to boost its low-carbon business amid growing interest in biogas.

Shell Plc is my star buy here as it looks positive in terms of both the price distribution and the technical sentiment. On that basis we are buyers at market 2,22.5 and look for a push higher to 2587.5 and 2721.0 to recover old ground. The stop loss is set at 2,204.80

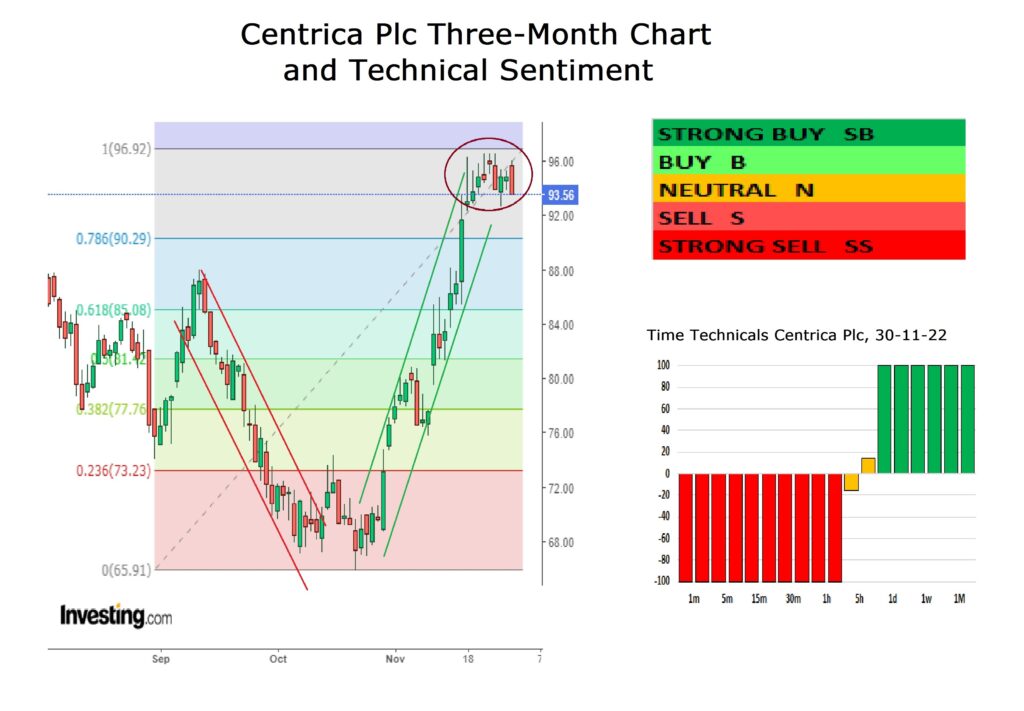

Centrica Plc is a British multinational energy and services company with its headquarters in Windsor, Berkshire. Its principal activity is the supply of electricity and gas to consumers in the UK and Ireland.

Centrica claimed on November 10 that earnings will be “…towards the top end of the range…” of analysts’ expectations and as such it saw no problem in launching a buyback of 5% of the share capital, which will cost roughly GBP 250 Million. The shares rose 6% on that news.

The company has been steadily filling its storage facilities in advance of any supply disruptions in a determined effort to retain its position as the largest energy supplier to households in the UK, with over 7 Million customers.

However, like any entity that derives an income from trading in fossil fuel products it has a strong eye to the future and the drive toward net zero. Last year the firm launched its Climate Transition Plan, which sets out a roadmap to establish itself as a net zero business by 2045 and to help transition its customers do so by 2050.

This is a stock that I am not buying right away as the impulsive channel is breaking down and the technical sentiment is not going to turn until later this week. I will make a small entry between 90.29 and 90.50 to test if the price has scope for a new push. On a failure my stop is set at 88.00 as that may well signal a deeper setback toward 85.08.

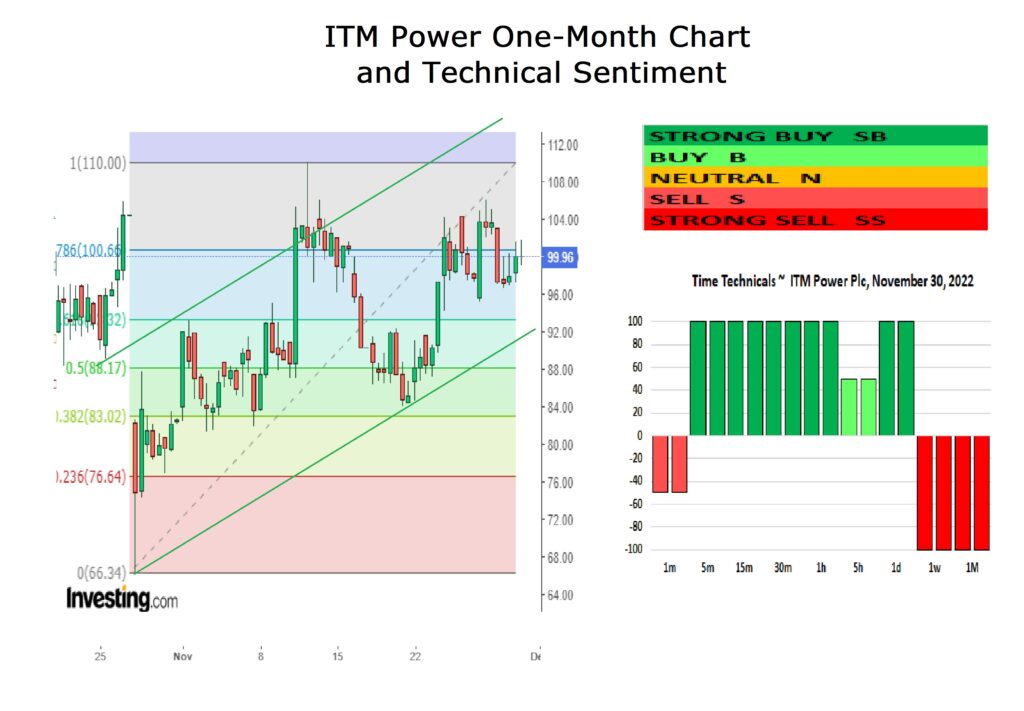

ITM Power Plc is an energy storage and clean fuel company founded in the UK in 2001. It designs, manufactures, and integrates electrolysers based on proton exchange membrane technology to produce green hydrogen using renewable electricity and tap water.

The past weekend edition of the FT it was reported that ITM Power Plc was a former market darling that has shed over 70% of its market value this year and had to seek a new CEO.

Dennis Schulz became CEO in December 2022, joining from Linde Engineering in Dresden, Germany, where he acted as Managing Director since 2020. He brings with him over 14-years of experience working with Linde Engineering across a wide variety of functions including project execution, Head of Strategy and CFO.

Prior to joining ITM Power, he was closely involved in Linde’s strategic relationship with ITM Power and has been a key figure in the green hydrogen economy and is passionate about industrial decarbonisation.

The demand for hydrogen reached an estimated 87 million tonnes in 2020 and is expected to grow to 500–680 Million Tonnes by 2050. In 2021 the hydrogen production market was valued at USD 130 Billion and is forecast by The World Bank to grow up to 9.2% per year through 2030.

It is a puzzle as to why the hydrogen market has not taken off as net zero plans appear to be favoured by RePowerEU and the Inflation Reduction Act. The current problem is that over 95% of current hydrogen production is fossil-fuel based. In short, not much of it is environmentally friendly. Today, 6% of global natural gas and 2% of global coal go into hydrogen production.

That said, green hydrogen production technologies are seeing a renewed wave of interest if it can develop an economy of scale.

ITM Power has found that developing scalable hydrogen technology is costly. That coupled with a delayed project of installing increased electrolyser capacity in Germany means revenues will be down in 2023 cf. this year. To alleviate liquidity concerns, the group has high hopes that the JV with Linde of Germany will allow its engineering, procurement and construction to be sold.

ITM Power announced in October that manufacturing issues mean revenue for the current year “…is likely to be towards the bottom of the current guidance range…”.

This means investors will ask if ITM Power is able to scale up its manufacturing and commercialisation efforts. One could ask why I am even looking at this company as it appears to be nothing less than a cash drain? This is a potential investment for the patient, deep pocketed investor that may say so much of the energy market is overvalued and they want an opportunity for a speculative venture.

I did not show the three-month chart as it would yield little information about near-term price recovery potential. The technical sentiment is highly mixed although in the next day or so there may be opportunities for a quick push to 110.00 and perhaps 120.00.

This may prove to be a stock where one has to be an active day trader, ready to trade in and out quickly. Only the individual investor can determine if they wish to dedicate such an allotment of time.

Top Investing Takeaway

It is an ill wind that bears no-one any good.

In the winter we all consume more energy to simply keep warm. So, when the OECD said on Tuesday, November 29 that Europe will bear the brunt of a global economic slowdown as energy prices soar and business activity wanes due to Russia’s war in Ukraine, it is not bad news all round.

Where to invest? Just follow the scent of the money for even though the European economic outlook is gloomy, on Tuesday, as the OECD made its statement, across the Euro Stoxx 600, the biggest gains were seen in the energy and mining sectors, with oil and gas firms leading the charge.