One answer to that headline question – UK Energy prices, what’s up? – is that UK energy prices are up, that’s what. But that’s not a grandly illuminative statement as most of us have seen our own bills where this is true. And, of course, what most of us want to know is what happens next?

It’s also true that we’d like to know this for two reasons. Firstly, as consumers of that energy we’d like to know when we can all stop shivering in the dark. Secondly, as investors, we’d like to know where we should be putting our money to take advantage of the price changes.

UK Energy market details

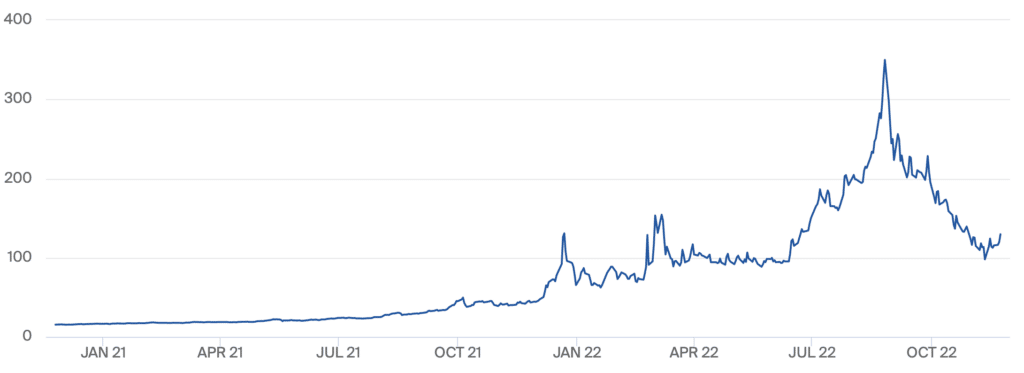

The microeconomics of markets first. The vast rise in energy prices caused by the disappearance of Russian gas from the European markets has happened. Prices have peaked and declined again. We can look at Dutch TTF (one of the many European natural gas prices) if we like, prices are back to where they were in February. The same is true of the Austrian gas futures (another European contract). This is pretty much true of all energy contracts – prices jumped, vastly, with the uncertainty of war and supply disruptions. Then everyone realised that a) markets are pretty good at dealing with this and b) one of the reasons why is that consumers will, in the face of vast price rises, use less energy.

Now, whether this will all stay as it is depends on how bad the winter is more than anything else. But at least at present the vast prices of the summer are gone. It’s entirely possible – not wholly likely, but possible – that power bills won’t in fact even meet the supposed upper limits that the government is subsidising.

UK Energy market investments

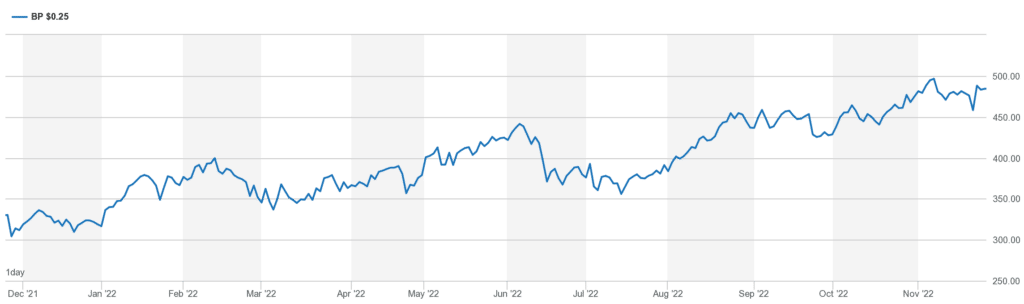

But we also want to know as investors – where’s the game for us and our money rather than us and our cardigans? So, we can look at energy suppliers in general: BP (LON: BP.) say. But sadly, we have a couple of problems here – it’s not so simple. Yes, high prices lead to high profits for energy producers. But if we look at the detail for BP then we find that a goodly chunk of profits came from price volatility – they run possibly the savviest gas trading desk in the world after all. High and volatile are not quite the same thing in this world. Then we’ve our second problem which is a Chancellor hungry for revenue. We’ve already got a windfall tax which, given that BP produces not all that much domestically, doesn’t matter all that much so far. But that could change. We have added political risk that is.

UK energy market political risk

Or we could look slightly differently at this and think about someone who works more nearly purely domestically. If UK energy prices are up, then someone who produces UK energy domestically and sells UK energy domestically could do well. Especially if their sales prices are up but not their production costs. SSE (LON: SSE) fits that bill pretty well. They’ve a vast wind farm arm, costs for that haven’t risen, but sales prices have. Except there we face that political risk again. That windfall tax has just been extended to the non-fossil fuel providers. So, while profits are up those attributable to shareholders aren’t so much.

Markets are difficult things, right, especially when politics gets involved?

UK energy market investment takeaways

So, what we really want to know about UK energy prices is not what’s up? But what’s going to happen next?

It’s not possible to know what’s going to happen next of course. But we can sketch out likely scenarios. In the short-term energy prices are going to vary with the weather – a cold snap will drive them up, likely substantially. In the medium to long-term they’re likely to moderate. Not because of any miracle of markets but because that’s just the way they do work. High prices generate supply and curb demand and so lower prices again.

For shares involved in energy supply we can expect those significant profit margins to continue. But how much of that filters through to shareholders will depend, as ever, on the level of the windfall tax – how much do the politicians think they should have instead.

The major determinant of British energy investment prices is thus going to be British politics. The major short-term determinant of global such prices the weather and then, in the medium term, the war itself and reactions to it. These aren’t forecastable events, but they are the ones it will be necessary to react to.