Macroeconomic/ geopolitical developments

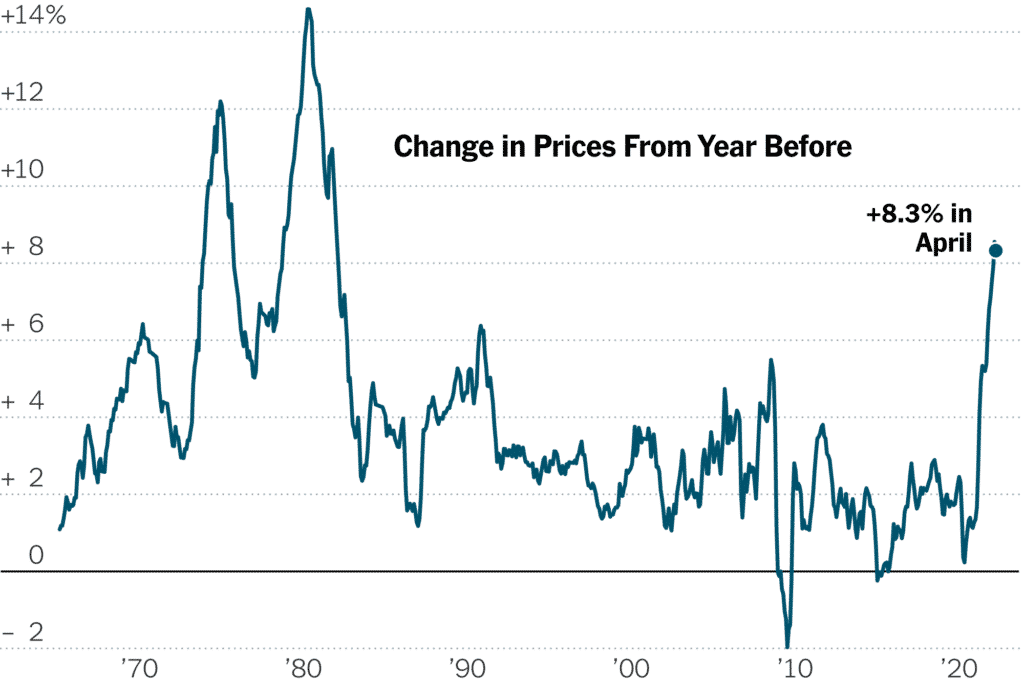

- US CPI headline data year over year rose 8.3%, falling from March’s pace but not as much as expected, with consensus around 8.1%.

- Jerome Powell again stated that a hike of 0.75% was not something being actively considered, but was still a possibility.

- Possible easing of pandemic lockdowns in Shanghai, China brought some cheers to Chinese and Asian stocks, slightly easing global supply chain and inflation worries.

Global financial market developments

- Six consecutive down weeks for the S&P 500 Index and the Nasdaq Composite and seven for the Dow Jones Industrial Average, its longest losing stretch since 2001!

- But rebound efforts from the latter part of the week have hinted at basing patterns.

- Global stock averages were also initially lower last week, although European and UK indices did rebound and are still outperforming their US counterparts.

- US 10yr yields broke back below the psychosocial 3% barrier as US and global bonds move to lower yields.

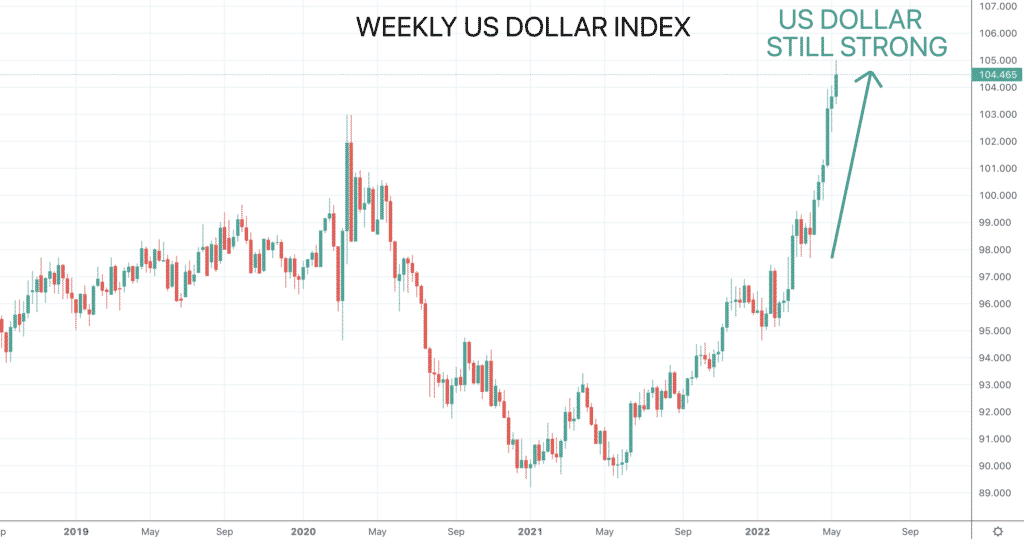

- US Dollar strength has extended as the greenback stays strong across the board.

- Gold sold off further with USD gains, staying more bearish.

- Oil moved higher again, reinforcing a positive range environment.

- Copper pushed still lower for a still more negative tone, but a bounce does hint at a base.

Key this week

- Geopolitical focus: Still closely monitoring the war in Ukraine

- Central Bank Watch: A light week for Central Banks, we get the Reserve Bank of Australia (RBA) Meeting Minutes on Tuesday and Jerome Powell also speaks Tuesday, then the People’s Bank of China (PBoC) interest rate decision on Friday.

- Macroeconomic data: A light week for data, with the US Retail Sales data and UK Employment reports the standouts on Tuesday.

| Date | Key Macroeconomic Events |

| 16/05/22 | China Retail Sales |

| 17/05/22 | RBA Meeting Minutes; UK Employment report; EU GDP; US Retail Sales; Jerome Powell speaks |

| 18/05/22 | UK CPI; Canada CPI |

| 19/05/22 | Australian Employment report |

| 20/05/22 | PBoC interest rate decision |