Macroeconomic/ geopolitical developments

- U.S. stocks ended the week higher, with the Nasdaq up 2.6%, the S&P 500 up 1.5%, and the Dow up 0.5%, rebounding from early losses as growth stocks outperformed, bond yields fluctuated, and global markets rallied amid easing tariff concerns and resilient investor sentiment.

- Markets remained resilient despite the announcement of 25% tariffs on imported steel and aluminum, as investors took comfort in the delay of reciprocal tariffs, leading to a stock rebound, a dip in the U.S. dollar, and eased concerns over trade-related inflation.

- Federal Reserve Chair Jerome Powell emphasized a patient stance on interest rates, citing persistent inflation above the 2% target and economic strength as reasons to delay cuts, while leaving the door open for prolonged policy restraint amid trade uncertainties.

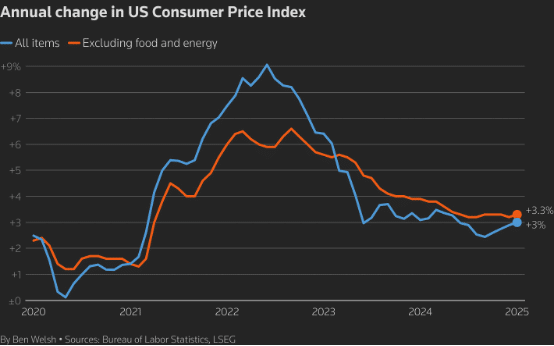

- U.S. inflation rose more than expected in January, with consumer prices increasing 0.5% month-over-month and 3% annually, prompting traders to push back expectations for Fed rate cuts while policymakers weigh persistent price pressures against economic uncertainty.

- Investors will analyze the Federal Reserve’s January meeting minutes on Wednesday for interest rate guidance, while key economic data, including PMI surveys and housing market reports, will provide further insights into U.S. economic momentum in a holiday-shortened week.

Global financial market developments

- US and global equity averages extended higher

- US and European bond were little changed on the week

- The US Dollar Index moved lower.

- Gold futures rallied, to a new all time high, before setting back.

- Oil futures consolidated, but remains negative short-term.

Key this week

Central Bank Watch: The main central bank activity this week is the Federal Open Market Committee Minutes on Wednesday. Some other activities of note are the Reserve Bank of Australia Interest Rate Decision and Monetary Policy Statement on Tuesday and the People’s Bank of China Interest Rate Decision on Thursday.

Macro Data Watch: The main macro data release this week is the Global Flash PMI on Friday. Some other releases of note are the Japanese GDP on Monday, Canadian CPI on Tuesday, UK CPI, PPI and RPI on Wednesday and Japanese CPI on Friday.

Data table on next page.

| Date | Major Macro Data |

| 02/17/2025 | US Presidents’ Day Holiday, markets closed; Japanese GDP |

| 02/18/2025 | RBA Interest Rate Decision and Monetary Policy Statement; UK Employment Report; Canadian CPI |

| 02/19/2025 | Japanese Trade Report; UK CPI, PPI and RPI; FOMC Minutes |

| 02/20/2025 | PBoC Interest Rate Decision; German PPI; EU Consumer Confidence |

| 02/21/2025 | Global Flash PMI; Japanese CPI; UK Consumer Confidence and Retail Sales; Canadian Retail Sales |