Macroeconomic/ geopolitical developments

- US and global bond markets went further into free fall last week, as yields surge to yet further multi-year highs, as stagflation fears and the “higher for longer” mantra persists.

- US and global PMI data from S&P Global and the ISM in the US was broadly better than expected for both Manufacturing and Services

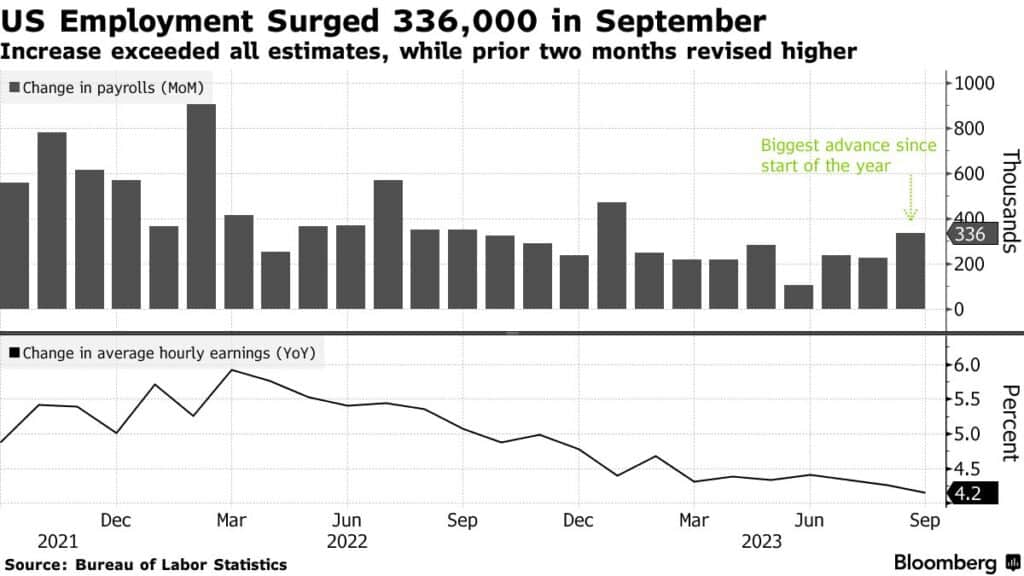

- The US employment data was released on Friday and notably beat consensus data, with 336K jobs added and significant positive revisions for July and August, to 236K and 227K, respectively.

Global financial market developments

- US and global equity index futures dipped last week, but then bounced on Friday after the US Employment report, hinting at a base.

- US and global yields surged even higher, with USTs hitting even higher multi-year highs.

- The US Dollar Index pushed higher, to then set back from new multi-month highs.

- Gold futures plunged still lower, with only a modest rebound Friday.

- Oil futures plunge, reversing September bullish forces, with the risks now lower.

Key this week

A quiet start to the week, with the US Columbus Day holiday on Monday, US cash bond markets are closed, plus it is Thanksgiving Day in Canada.

Central Bank Watch: A quiet week for central banks, with the main focus on the release of the FOMC Minutes on Wednesday.

Macroeconomic Data: Key data for the week will be German and EU Industrial Production, plus UK GDP, Industrial and Manufacturing Production, plus German CPI. But critical data will be Thursday’s US CPI release.

| Date | Key Macroeconomic Events |

| 10/09/2023 | US Columbus Day holiday, US cash bond markets are closed; Thanksgiving Day Canada; German Industrial Production |

| 10/10/2023 | Little of note |

| 10/11/2023 | German CPI; US PPI, FOMC Minutes released |

| 10/12/2023 | UK GDP, Industrial and Manufacturing Production; US CPI; |

| 10/13/2023 | China CPI and trade data; EU Industrial Production; Michigan Consumer Sentiment Index |