Macroeconomic/ geopolitical developments

- This past week has been all about frenzied stock market exuberance, often a reflection of an inflating equity market “bubble” and the fears and concerns that this activity brings.

- GameStop shares have skyrocketed in the past week having already seen an aggressive rise in January, driven by a herd mentality of individual traders, buoyed by Reddit posts, particularly from WallStreetBets.

- The tactic was to push the stock higher, as there were “crowded”, leveraged shorts amongst hedge funds, who were looking for the stocks to fall in value (given already weakened company prospects even before the pandemic).

- See our article here on leverage or margin trading.

- Many of these hedge fund shorts, with the most highlighted being Melvin Capital, have been put under financial pressure due to the aggressive buying from the individual targets working as a herd.

- GameStop shares surged 400% for the week and 1600% for January, with other stocks such as AMC also pushing aggressively higher in a similar move.

- In turn, this saw many brokers, most prominently the Robinhood trading app, suspend trading in certain stocks, as the brokers needed to draw on credit lines as they themselves faced margin issues.

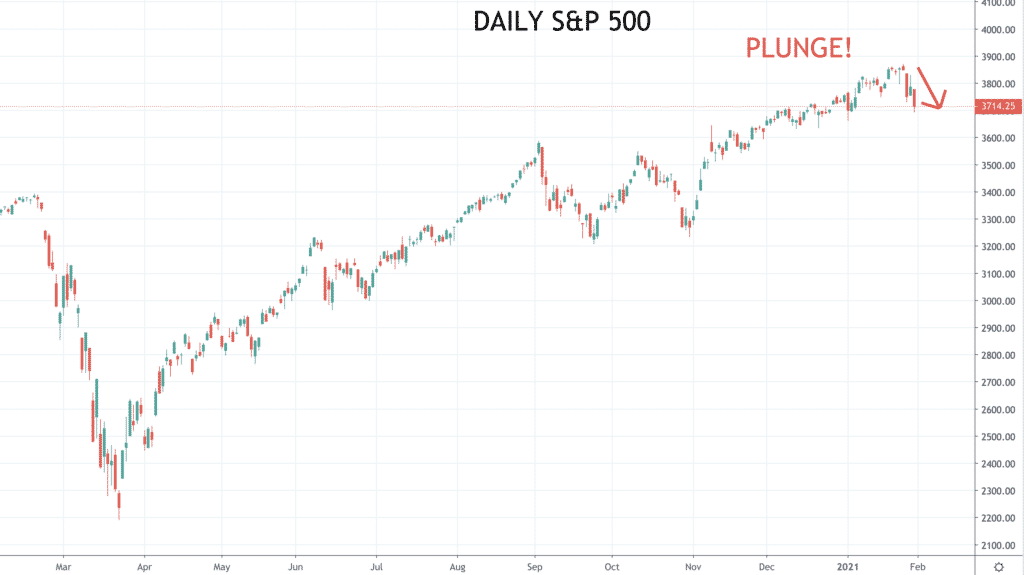

- This impacted the broader market in a negative way, with a plunge in the major stock indices.

- This was driven by two factors; aforementioned hedge fund shorts in these stocks, liquidating positions in the broader market to repay stock loans and wider fears that this activity is a reflection of an over exuberant market.

- The Federal Reserve Open Market Committee (FOMC) rate decision, Statement and Press Conference came and went on Wednesday with little market impact.

- Earnings season saw a busy week but the impact on the wider market was not particularly significant. Apple, Facebook and Tesla all reported strong numbers, although Tesla did miss on earnings/ share, whilst forward guidance from Facebook and to an extent from Apple was not overly positive.

- The slow rollout of vaccines in Europe has seen some countries run out of vaccine, with this issue becoming politicised as the EU have looked to restrict exports of vaccines.

- Lockdown measures in parts of Europe are being added to, with travel restrictions being further tightened.

- The spread of new variants of COVID-19 has seen cases, hospitalisations and deaths rise in 2021, though the more recent lockdown measures have started to have a positive impact in some countries in Europe over the past week.

Global financial market developments

- The major global equity indices plunged lower last week, as US averages joined their European counterparts in breaking key technical support levels.

- The US Dollar extended its rebound from its weak 2020 position, building on gains from earlier in January, signalling upside risks for the US currency.

- The US currency made notable gains versus the Japanese Yen AND the Australian Dollar.

- The British Pound stays particularly strong, with GBPUSD prodding to yet another new multi-year high last week (though is showing modest signs of vulnerability.

- In the commodity space, Oil has been sideways since mid-January, but with risks skewed towards a correction lower.

- Copper remains in a negative consolidation phase since early January, again with the asymmetric bias lower.

- Gold has been sideways for two weeks but stay vulnerable since the earlier January plunge lower.

Key this week

- Geopolitics:

- Will the US Securities Exchange Commission (SEC), the UK Financial Conduct Authority (FCA) or other authorities in Europe and elsewhere step in to investigate the frenzied activity seen in some stocks, as highlighted above?

- Traders should monitor further executive orders from President Biden.

- Watching for new lockdown measures, in the US and Europe (or the removal of measures).

- COVID-19 cases, hospitalisations and deaths stay in focus in US and Europe.

- Markets will be waiting for further vaccine delivery developments and vaccine approvals.

- Central Bank Watch: Tuesday brings the Reserve Bank of Australia (RBA) interest rate decision, Statement and Press Conference and on Friday their Monetary Policy Statement, with the Bank of England (BoE) interest rate decision, Statement and Press Conference on Thursday.

- Macroeconomic data: Standout data this week are the Global Markit Manufacturing PMI and US ISM Manufacturing PMI on Monday and the equivalent for the Services and Composite on Wednesday, then the US Employment report on Friday.

- Microeconomic data: US earnings season continues, with standouts this week being; Amazon, Google (Alphabet), Pfizer, Exxon Mobil, PayPal and Merck & Co.

| Date | Key Macroeconomic Events |

| 01/02/21 | Global Markit Manufacturing PMI and US ISM Manufacturing PMI; German Retail Sales |

| 02/02/21 | RBA interest rate decision, Statement and Press Conference; Eurozone GDP |

| 03/02/21 | New Zealand employment; global Markit Services and Composite PMI and US ISM Services PMI; Eurozone CPI; US ADP employment |

| 04/02/21 | BoE interest rate decision, Statement and Press Conference; Eurozone Retail Sales; US weekly Jobless Claims |

| 05/02/21 | RBA Monetary Policy Statement; US and Canadian employment reports |